Though 2023 was a stellar yr for the inventory market, volatility has been the secret for a lot of the previous 4 years. The Dow Jones Industrial Common, S&P 500, and Nasdaq Composite have oscillated between bear and bull markets in successive years since this decade started.

When volatility picks up on Wall Avenue, skilled and on a regular basis traders tend to hunt out firms that provide a historical past of outperformance. For the previous two and a half years, it is shares enacting splits which have match the invoice.

In easy phrases, a inventory cut up is an occasion that enables a publicly traded firm to change its share worth and excellent share depend whereas having no affect on its market cap or operations. Consider it as a purely beauty process that may make shares extra nominally reasonably priced for retail traders (i.e., a forward-stock cut up), or can enhance a publicly traded firm’s share worth to make sure continued itemizing on a significant inventory change (i.e., a reverse inventory cut up).

Whereas there are cases of firms conducting reverse-stock splits and happening to ship big-time positive factors for his or her shareholders (e.g., Reserving Holdings), most traders are laser-focused on firms conducting forward-stock splits. That is as a result of ahead splits are enacted by high-flying firms which have typically out-innovated and handily out-executed their competitors.

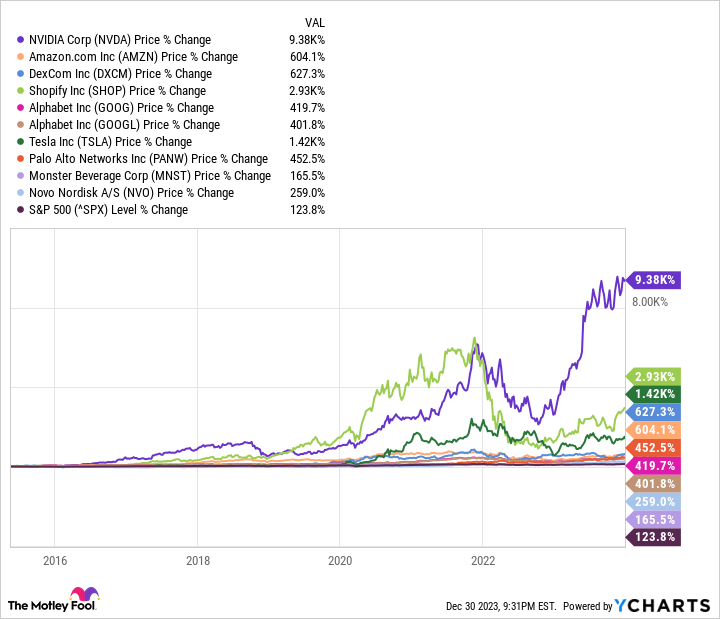

For the reason that midpoint of 2021, 9 outstanding firms have accomplished a forward-stock cut up:

-

Nvidia (NASDAQ: NVDA): 4-for-1 cut up

-

Amazon (NASDAQ: AMZN): 20-for-1 cut up

-

DexCom (NASDAQ: DXCM): 4-for-1 cut up

-

Shopify (NYSE: SHOP): 10-for-1 cut up

-

Alphabet (NASDAQ: GOOGL)(NASDAQ: GOOG): 20-for-1 cut up

-

Tesla (NASDAQ: TSLA): 3-for-1 cut up

-

Palo Alto Networks (NASDAQ: PANW): 3-for-1 cut up

-

Monster Beverage (NASDAQ: MNST): 2-for-1 cut up

-

Novo Nordisk (NYSE: NVO): 2-for-1 cut up

Each single certainly one of these companies is a dominant participant with well-defined aggressive benefits of their respective industries. For instance, Nvidia’s graphics processing models are the infrastructure spine of the synthetic intelligence (AI) motion, Amazon accounts for roughly 40% of U.S. on-line retail gross sales, Tesla is North America’s main electrical car (EV) producer, and DexCom is a top-two producer of steady glucose monitoring techniques.

Nevertheless, the person outlooks for these 9 stock-split shares differs significantly in 2024 (and past). Whereas one stock-split inventory is traditionally cheap and primed for added upside, one other highflier seems to be headed for a breakdown.

The stock-split inventory to purchase hand over fist in 2024: Alphabet

Although all 9 of those outstanding firms have run circles across the benchmark S&P 500 over the long term, it is Alphabet that stands out because the stock-split inventory to purchase hand over fist within the new yr. Alphabet is the father or mother firm of common web search engine Google and streaming platform YouTube.

The largest “drawback” (if you wish to name it that) for Alphabet is that it is cyclical. Roughly 78% of the corporate’s third-quarter income is derived from promoting. When the slightest trace of hassle is detected by companies, it is not unusual for them to shortly pare again their advert spending. This leaves Alphabet prone to weak spot throughout recessions. A few money-based metrics and predictive instruments counsel an financial downturn is within the playing cards for 2024.

Nevertheless, it is a two-sided coin that is removed from proportionate. Although it is true that recessions are a wonderfully regular and inevitable a part of the financial cycle, solely three of the 12 recessions because the finish of World Conflict II have lasted a minimum of 12 months. Additional, not a single one has surpassed 18 months.

By comparability, most financial expansions endure a number of years, with two durations of post-World-Conflict-II development lasting greater than a decade. Briefly, ad-driven companies are nicely positioned to succeed because the U.S. financial system expands.

Alphabet’s clearest aggressive benefit has lengthy been its search engine, Google. In November, Google totaled 91.54% of worldwide search share, in keeping with information from GlobalStats. You’d have to return to March 2015 to search out the final month Google hasn’t accounted for a minimum of 90% of worldwide web search share. Being the undisputed go-to for advertisers wanting to achieve customers has afforded the corporate distinctive ad-pricing energy in just about any financial local weather. This moat is not going away in 2024.

The brand new yr also needs to function double-digit development alternatives for 2 of Alphabet’s fast-growing ancillary segments. YouTube is the second most visited social web site on this planet, with greater than 2.7 billion month-to-month lively customers. Fast development in Shorts (short-form movies typically lasting lower than 60 seconds) ought to put ad-pricing energy in YouTube’s nook.

There’s additionally Google Cloud, which has devoured up a ten% share of worldwide cloud infrastructure service spending, based mostly on estimates from Canalys, as of the third quarter. Enterprise cloud spending nonetheless has a protracted development runway, and Google Cloud seems to be to have made the everlasting shift to recurring profitability.

Regardless of sustained double-digit earnings development potential over the subsequent 5 years (if not nicely past), Alphabet inventory could be bought for roughly 14 instances estimated money stream per share in 2024. That is a 20% low cost to its common a number of to money stream over the previous 5 years.

The stock-split inventory value avoiding in 2024: Tesla

To cite essentially the most well-known funding disclaimer on Wall Avenue: “Previous efficiency isn’t any assure of future outcomes.” Though EV maker Tesla has made a behavior of proving naysayers incorrect for greater than a decade, it is the clear stock-split inventory to keep away from in 2024 for quite a lot of causes.

Earlier than digging into these causes, enable me to present credit score the place credit score is due. As of proper now, Tesla is the one pure-play EV producer that is worthwhile on a recurring foundation. Whereas there are different worthwhile automakers, not one of the legacy firms are producing a recurring revenue from their electric-only divisions. When Tesla studies its fourth-quarter working outcomes, I might anticipate it to wrap up its fourth consecutive yr of typically accepted accounting rules (GAAP) revenue.

Sadly for the world’s largest automaker by market cap, its first-mover benefits are starting to wane, and there are very evident cracks in its basis.

Essentially the most front-and-center proof that Tesla is in hassle could be seen through its working margin, which has been greater than halved to 7.6% over the trailing yr, ended Sept. 30.

In 2023, North America’s main EV firm slashed costs on Mannequin’s 3, S, X, and Y on greater than a half-dozen events. Based mostly on feedback supplied by CEO Elon Musk throughout the firm’s annual shareholder assembly in Might, these worth cuts have been based mostly solely on demand. With car stock ranges rising, it is plainly evident that demand for the corporate’s EVs has declined. It additionally means that extra worth cuts could also be essential to preserve stock ranges below management as Tesla continues to ramp up its manufacturing.

One other potential drawback with Tesla is the way it’s deriving its earnings. Through the third quarter, Tesla booked $554 million in revenue from promoting renewable vitality credit given to it free of charge by governments. It additionally generated $282 million in curiosity earnings from its sizable money pile. That is $836 million in pre-tax earnings — 41% of the corporate’s pre-tax earnings within the third quarter — that may be traced again to unsustainable sources.

Though Elon Musk is a giant purpose Tesla has been so successful since going public in 2010, he is additionally a real legal responsibility for shareholders. Placing apart that he is drawn the eye of securities regulators on a few events, his largest flaw is that he often overpromises new improvements (together with new EVs) and fails to ship them. Tesla’s huge valuation seems to be to be based mostly on numerous guarantees from Musk that stay unfulfilled.

Lastly, Tesla’s efforts to change into greater than a automotive firm have largely missed the mark. Its ancillary segments generate low margins, whereas auto margins proceed to fall. Whereas most auto shares commerce between 6 and eight instances forward-year earnings, Tesla is valued at 65 instances consensus earnings in 2024. That is not a valuation that is going to carry up within the face of a quickly declining working margin.

Do you have to make investments $1,000 in Alphabet proper now?

Before you purchase inventory in Alphabet, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Alphabet wasn’t certainly one of them. The ten shares that made the lower might produce monster returns within the coming years.

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

See the ten shares

*Inventory Advisor returns as of December 18, 2023

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. Sean Williams has positions in Alphabet and Amazon. The Motley Idiot has positions in and recommends Alphabet, Amazon, Reserving Holdings, Monster Beverage, Nvidia, Palo Alto Networks, Shopify, and Tesla. The Motley Idiot recommends DexCom and Novo Nordisk. The Motley Idiot has a disclosure coverage.

1 Inventory-Break up Inventory to Purchase Hand Over Fist in 2024 and 1 to Keep away from was initially revealed by The Motley Idiot