Nvidia (NASDAQ: NVDA) embodies synthetic intelligence (AI) enthusiasm in contrast to some other development inventory. However what in the event you already personal sufficient Nvidia, or are merely in search of different alternatives?

A very good place to start out is by wanting on the corporations that Nvidia companions with that not directly profit from its success.

Three that stick out are Micron Expertise (NASDAQ: MU), Vertiv Holdings (NYSE: VRT), and Taiwan Semiconductor Manufacturing (NYSE: TSM). Here is what makes every inventory an ideal purchase now.

Micron is offering a key ingredient in Nvidia’s new GPU

Scott Levine (Micron Expertise): Of the various Nvidia companions which have the potential to prosper from a relationship with the AI juggernaut, Micron is an organization that ought to actually be on development traders’ radars.

A frontrunner in reminiscence and storage options, Micron benefited from the AI trade’s speedy development in 2023. Its new partnership with Nvidia means that the corporate is extraordinarily effectively positioned for future development because the AI market continues to soar.

In February, Micron introduced that it had commenced large-scale manufacturing of its excessive capability reminiscence resolution, the Excessive Bandwidth Reminiscence 3E (HBM3E), and it started deliveries of the product within the second quarter. Micron asserts that the HBM3E will assist allow “lightning-fast information entry for AI accelerators, supercomputers, and information facilities.” Nvidia will use the HBM3E in its graphics processing card (GPU), the H200 Tensor Core GPU. It is not solely a rise in efficiency that makes the HBM3E engaging — it is also interesting from an economics perspective. Micron lauds the HBM3E as a cheaper choice, because it makes use of 30% much less energy than comparable merchandise.

Based on Nvidia, the H200 Tensor Core GPU doubles the reminiscence capability of its earlier product, the H100 Tensor Core GPU, and has 1.4 occasions the bandwidth. With this improve in efficiency, Nvidia is assured that the H200 Tensor Core GPU will additional facilitate the event of generative AI and enormous language fashions.

The connection between Micron and Nvidia transcends the lately introduced collaboration. In fiscal 2019, for instance, Nvidia launched the GeForce RTX graphics card for the gaming market, which relied on Micron’s reminiscence chips.

Vertiv inventory nonetheless has upside potential

Lee Samaha (Vertiv Holdings): The information heart tools supplier’s inventory is on an unbelievable run. Up 549% during the last yr and 103% in 2024 alone, traders should be questioning simply how for much longer the inventory has to run, not least as a result of it trades at 41 occasions estimated 2024 earnings.

Sure, the valuation seems to be heady, however not if we’re solely within the very early innings of a multi-year funding cycle in information facilities pushed by AI-related funding. Vertiv’s digital infrastructure know-how (energy administration, thermal administration, rack techniques, and so forth.) is vital to the functioning of knowledge facilities, and it is a resolution advisor or advisor companion within the Nvidia companion community.

As such, it is a very important beneficiary of the increase in spending on AI, and the corporate’s current first-quarter earnings demonstrated the power of the momentum within the pattern. Its orders development was up 60% from the primary quarter of 2023, and its book-to-bill ratio was 1.5 occasions, implying vital income development to come back as the corporate executes on its $6.3 billion backlog.

Wall Road has Vertiv’s free money stream rising at 22% and 25% within the years after 2024, and if AI spending traits proceed, Vertiv ought to be capable of develop into its valuation. If you’re bullish on Nvidia, it is smart to have a look at Vertiv, too.

The linchpin of chip manufacturing

Daniel Foelber (Taiwan Semiconductor): Taiwan Semi is a guess on sustained demand for chips for client electronics, the automotive trade, AI accelerators, and extra. In 2023, the chip-making firm commanded 61% of world chip-foundry exercise.

Nvidia, Broadcom, Superior Micro Units, Qualcomm, and others depend on Taiwan Semi to take their proprietary designs and manufacture to extraordinarily exact specs. To not put down building or engineering contractors, however what Taiwan Semi is doing is a few of the most complex manufacturing on the earth. Taiwan Semi’s potential to meet advanced orders is why corporations world wide outsource their chip manufacturing to Taiwan.

Traders might wish to contemplate Taiwan Semi as a catch-all option to guess on the rising tides of AI, electrification, information facilities, and the overall want for extra computing energy. Taiwan Semi ought to profit so long as general demand is rising. It would not notably care if AMD is taking market share from Nvidia or vice versa.

Regardless of its benefits, Taiwan Semi does have some dangers — specifically competitors and the necessity to simplify provide chains and localize chip manufacturing to cut back geopolitical threat. The CHIPS Act within the U.S., for instance, is eager on allocating billions to extend home chip manufacturing. Taiwan Semi has fabs within the U.S., however it’s nonetheless primarily manufacturing chips in Asia.

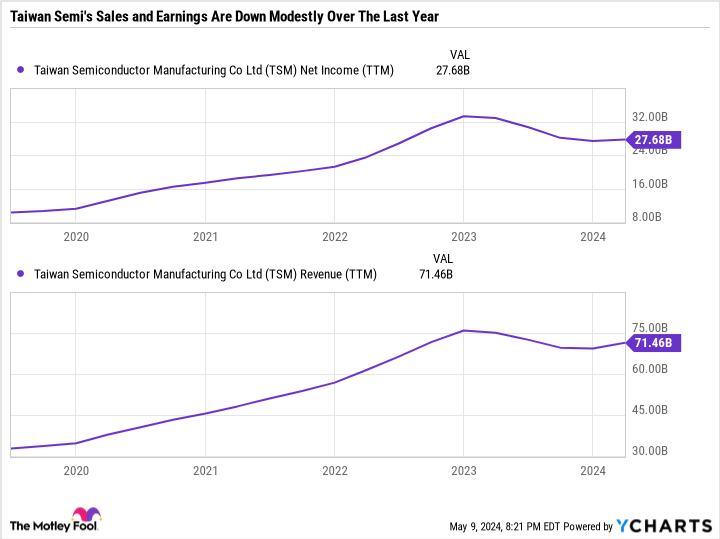

The tailwinds of AI are sturdy, however that does not imply that development within the semiconductor trade is a straight line up. Apple, for instance, is present process a slowdown pushed by weak iPhone demand. Taiwan Semi’s gross sales and earnings have flatlined lately as a few of its core markets fall below stress.

The excellent news is that analysts anticipate earnings to get well, with consensus estimates calling for $6.26 in 2024 earnings per share (EPS) and 2025 consensus estimates of $7.86. Consequently, Taiwan Semi’s ahead price-to-earnings (P/E) ratio is 22.7 in comparison with its present P/E of 27.2.

Regardless of being down simply 10% from its all-time excessive, Taiwan Semi is a good worth and a balanced purchase for traders with the endurance to endure the trade’s cyclicality. It additionally sports activities a 1.4% dividend yield as a cherry on high of the sturdy underlying funding thesis.

Must you make investments $1,000 in Micron Expertise proper now?

Before you purchase inventory in Micron Expertise, contemplate this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the 10 finest shares for traders to purchase now… and Micron Expertise wasn’t certainly one of them. The ten shares that made the reduce may produce monster returns within the coming years.

Take into account when Nvidia made this checklist on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $550,688!*

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of Might 13, 2024

Daniel Foelber has the next choices: lengthy July 2024 $180 calls on Superior Micro Units. Lee Samaha has no place in any of the shares talked about. Scott Levine has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Superior Micro Units, Apple, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Idiot recommends Broadcom. The Motley Idiot has a disclosure coverage.

3 Nvidia Companions With Explosive Development Potential to Purchase Now was initially printed by The Motley Idiot