Social Safety has been one of the vital necessary social packages within the U.S. for many years. For retirement particularly, it gives important revenue to hundreds of thousands of People throughout the nation. After years of paying Social Safety taxes, beneficiaries reap the rewards with a monetary security web of types.

Nonetheless, these advantages aren’t restricted solely to individuals who labored and paid taxes through the years. For instance, Social Safety permits spousal advantages to help non-working or low-earning spouses in retirement. For any couple that’s nearing or in retirement and placing monetary plans in place, listed below are three issues they need to find out about Social Safety spousal advantages.

1. How Social Safety spousal advantages work

Social Safety usually calculates a recipient’s month-to-month advantages utilizing a system that elements of their 35 highest-earning years of revenue. However a partner can obtain Social Safety advantages primarily based on their accomplice’s incomes file in the event that they’re at the least 62 years outdated or caring for a kid underneath 16 or with a incapacity.

Assuming the individual claiming spousal advantages is at full retirement age, they’re eligible to obtain 50% of their partner’s major insurance coverage quantity too.

For instance, if partner A’s earnings file provides them a month-to-month good thing about $2,000 at their full retirement age, partner B might obtain as much as $1,000 month-to-month as effectively. The precise quantity will depend upon the age at which partner B claims advantages.

2. The influence of claiming advantages early or late

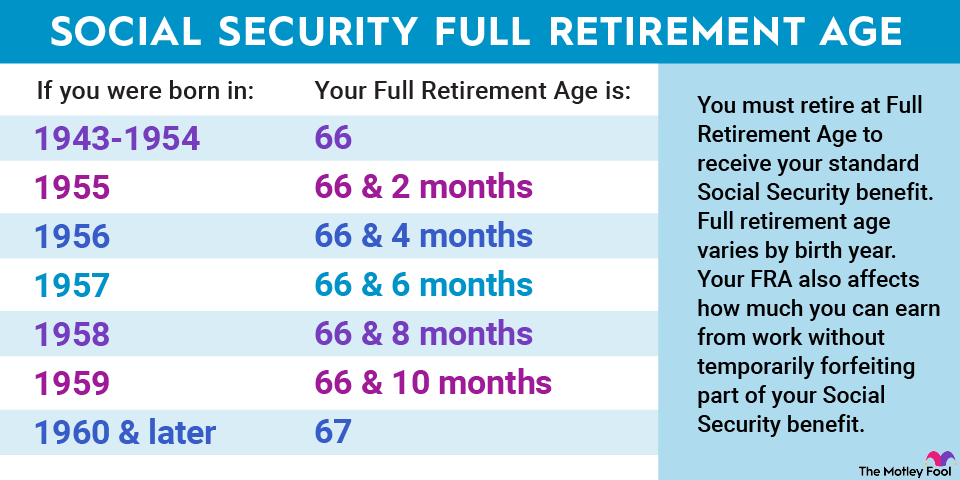

Your full retirement age is without doubt one of the most necessary numbers associated to Social Safety as a result of it tells you once you’re eligible to obtain your major insurance coverage quantity. Nonetheless, you do not have to assert advantages at your full retirement age; you may declare them early (which reduces your payout) or delay (which will increase your payout).

Claiming Social Safety advantages early impacts a partner and their accomplice receiving spousal advantages in several methods.

Trying first on the individual claiming primarily based on their work file, their advantages are diminished by 5/9 of 1% every month earlier than their full retirement age, as much as 36 months. Every month after that additional reduces advantages by 5/12 of 1%. Here is an instance: Somebody with a full retirement age of 67 who claims advantages at 62 will see their month-to-month profit diminished 30% from their major insurance coverage quantity.

For the individual receiving spousal advantages, advantages are diminished by 25/36 of 1% every month earlier than their full retirement age, as much as 36 months, after which they go down 5/12 of 1% every month thereafter. So an individual with the identical full retirement age (67) claiming spousal advantages at 62 would see their checks diminished 35%.

Though advantages usually enhance when you wait past your full retirement age, these delayed retirement credit do not apply to spousal advantages.

3. What occurs if a partner passes away

Social Safety spousal and survivors advantages may be intently linked because the latter extends vital monetary help after a accomplice has handed away.

For those who’re claiming spousal advantages when your accomplice passes away, Social Safety will convert your spousal advantages to survivors advantages. Survivors advantages make you eligible to obtain as much as 100% of your deceased partner’s profit, together with any delayed retirement credit they earned previous to their passing. A widow or widower can start receiving survivors advantages at age 60 (50 if coping with a incapacity), however as within the case with spousal advantages, they’re going to be diminished if claimed earlier than full retirement age.

You possibly can’t concurrently obtain spousal and survivors advantages, solely whichever is increased. Since spousal advantages max out at 50% of the accomplice’s major insurance coverage quantity, survivors advantages are usually the higher-paying possibility.

The $21,756 Social Safety bonus most retirees fully overlook

For those who’re like most People, you are a number of years (or extra) behind in your retirement financial savings. However a handful of little-known “Social Safety secrets and techniques” might assist guarantee a lift in your retirement revenue. For instance: one simple trick might pay you as a lot as $21,756 extra… annually! When you learn to maximize your Social Safety advantages, we predict you possibly can retire confidently with the peace of thoughts we’re all after. Merely click on right here to find find out how to study extra about these methods.

The Motley Idiot has a disclosure coverage.

Spousal Social Safety Advantages: 3 Issues All Retired {Couples} Ought to Know was initially printed by The Motley Idiot