AGNC Investments (NASDAQ: AGNC) pays an eye-popping dividend. At over 14%, it is practically 10x larger than the S&P 500‘s dividend yield (presently 1.5%).

Nonetheless, as engaging as that payout might sound, income-focused traders are higher off forgetting in regards to the mortgage REIT. They will probably make far more cash in different high-yielding shares, together with MPLX (NYSE: MPLX). This is why the 9.3%-yielding grasp restricted partnership (MLP) is a greater choice for these looking for a robust whole return (dividend earnings plus inventory value progress).

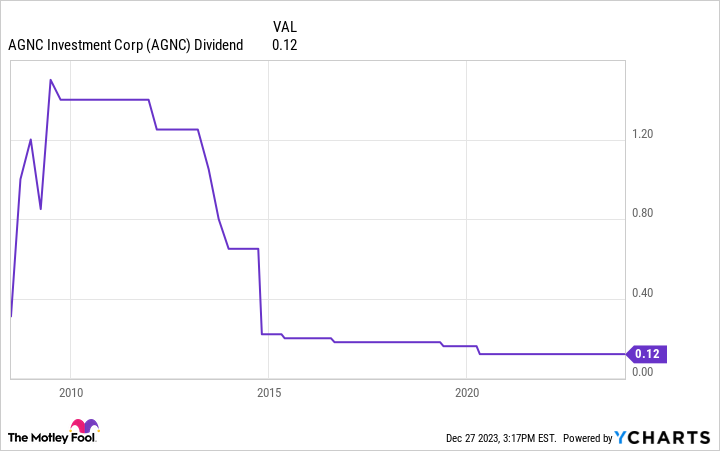

Not a really bankable dividend

Mortgage REITs like AGNC Investments have extra in frequent with banks than conventional REITs. As an alternative of proudly owning income-producing actual property, AGNC invests in mortgage-backed securities (MBS) assured by authorities companies. Whereas these ensures get rid of default threat, the REIT faces many different dangers that may influence its earnings stream.

The 2 greatest ones are interest-rate threat and reinvestment threat. Like a financial institution, AGNC Investments makes use of short-term borrowings to fund long-term investments, benefiting from the unfold between short- and long-term charges.

The issue with that is that rates of interest might be risky. An surprising charge change can drive up its funding prices, squeezing its revenue margin. In the meantime, falling charges permit debtors to refinance. After they do, AGNC receives its principal again and should reinvest it at a decrease charge.

Whereas this enterprise mannequin might be extremely worthwhile (therefore AGNC’s high-yielding payout), these earnings might be risky. That variability has compelled AGNC Investments to chop its dividend a number of instances through the years:

With charges anticipated to fall subsequent yr, AGNC would possibly want to chop its dividend once more.

The mortgage REIT’s falling dividend has weighed on its means to create worth for shareholders through the years. Its inventory has misplaced practically 50% of its worth over the previous decade.

Whereas the corporate’s high-yielding dividend has helped make up a few of that misplaced floor, it has solely produced a 68% whole return (5.3% annualized). That has considerably underperformed the S&P 500’s 213% whole return (12.1% annualized).

The gasoline to proceed rising

MPLX has a way more secure enterprise mannequin. The MLP operates midstream belongings (pipelines, processing crops, and storage terminals) that generate very regular money circulate backed by government-regulated charge constructions and long-term contracts with high-quality clients, together with its father or mother, refining-giant Marathon Petroleum.

The corporate had generated over $3.9 billion in money by the primary 9 months of this yr (a 6% improve from the year-ago interval). That simply coated its big-time distribution ($2.4 billion in whole money funds). That enabled the MLP to retain sufficient money to fund its capital bills ($727 million) with room to spare ($752 million in adjusted free money circulate).

That extra money strengthened its already fortress-like stability sheet. MPLX ended the third quarter with $960 million of money and a 3.4x leverage ratio (properly beneath the 4x vary its secure money circulate can assist).

In the meantime, the corporate’s growth-focused investments will assist improve its regular money circulate. MPLX presently has a number of growth initiatives beneath building that ought to come on-line over the following two years. That offers it seen cash-flow progress on the horizon. It additionally has the monetary energy to boost its natural progress by making acquisitions to spice up its money circulate.

The MLP’s progress drivers ought to give it the gasoline to proceed growing its distribution. It not too long ago raised its payout by one other 10% and has given traders a elevate yearly since Marathon created the corporate in 2012, rising the payout by greater than 200% general.

The corporate’s steadily rising payout has helped energy a lot larger whole returns than AGNC Investments. It has produced a greater than 200% whole return since its formation (10.4% annualized). With extra earnings and dividend progress forward, it ought to be capable of proceed making its traders more cash than AGNC Investments.

The gasoline to provide larger returns

AGNC Investments has steadily reduce its dividend through the years as interest-rate fluctuations weighed on its money circulate. With extra interest-rate volatility forward, the mortgage REIT may reduce its payout once more.

However, MPLX has steadily elevated its distribution through the years because it has grown its portfolio of cash-producing midstream belongings. With a number of growth initiatives presently underway, it ought to have the gasoline to proceed growing its distribution.

The chance of continued progress makes it a greater choice for earnings seekers. It ought to ship a steadily rising payout and produce larger whole returns than AGNC Investments over the long term.

Must you make investments $1,000 in AGNC Funding Corp. proper now?

Before you purchase inventory in AGNC Funding Corp., contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 finest shares for traders to purchase now… and AGNC Funding Corp. wasn’t one in every of them. The ten shares that made the reduce may produce monster returns within the coming years.

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

See the ten shares

*Inventory Advisor returns as of December 18, 2023

Matthew DiLallo has no place in any of the shares talked about. The Motley Idiot has no place in any of the shares talked about. The Motley Idiot has a disclosure coverage.

Overlook AGNC — This Extremely-Excessive-Yield Dividend Inventory Will Make You Far Extra Cash was initially revealed by The Motley Idiot