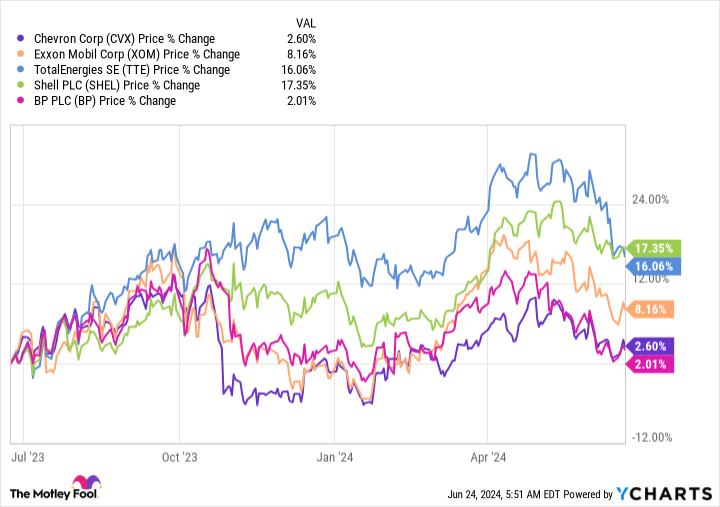

Chevron (NYSE: CVX) inventory has been in the back of the pack performance-wise over the previous 12 months, with a acquire of simply 2%. ExxonMobil (NYSE: XOM) is up 8% over that span, and Shell (NYSE: SHEL) has gained round 17%. However do not depend Chevron out in case you are wanting on the power sector. In actual fact, that laggard efficiency may truly make it probably the most enticing built-in power inventory you should buy at present.

What’s Chevron’s drawback?

The one phrase that ought to be on traders’ lips proper now might be “why.” As in, why is Chevron trailing different built-in power firms by such a large margin? One large a part of the reply is that Chevron lately inked an settlement to purchase Hess (NYSE: HES). However Hess is in a partnership with Exxon on a giant capital funding within the oil area. Exxon is trying to throw a wrench into Chevron’s acquisition by saying it might probably purchase Hess out of that partnership.

That may make Chevron’s acquisition a lot much less fascinating and will even result in the deal being canceled. One other drawback right here is that determining who’s proper might result in materials delays and may require some authorized wrangling, which might be pricey. This uncertainty has left a cloud over Chevron’s inventory, as traders usually don’t love uncertainty.

However that is not all unhealthy information, because it has left Chevron with a reasonably large dividend yield of 4.2% relative to its closest peer Exxon, which is yielding simply 3.4%. And whereas Exxon has elevated its dividend for 42 years, it’s arduous to complain about Chevron’s spectacular 37-year streak of annual dividend hikes. Merely put, they’re each dependable dividend shares.

Chevron is best ready for adversity

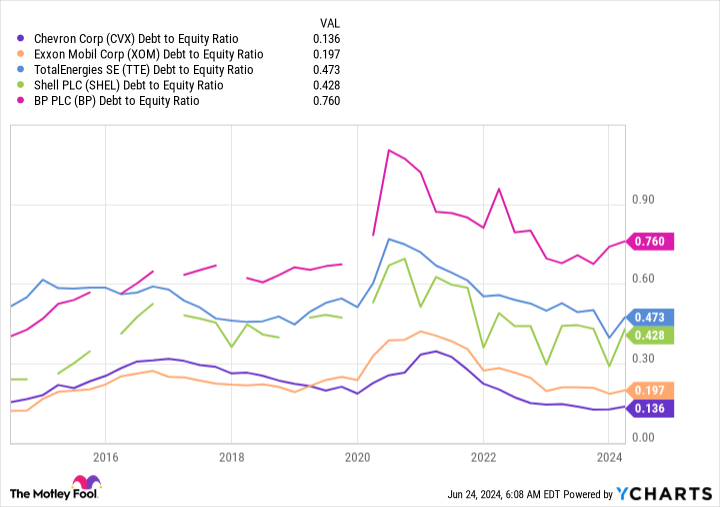

That mentioned, whereas Exxon is not financially weak by any stretch of the creativeness, Chevron is at the moment in a greater monetary place than any of its closest opponents. Notably, Exxon’s debt-to-equity ratio is roughly 0.2 occasions, whereas Chevron’s ratio is round 0.15 occasions. European friends make a lot larger use of leverage. Chevron has the strongest stability sheet amongst built-in power majors. Leverage is vital as a result of the power sector is very cyclical and susceptible to dramatic worth swings.

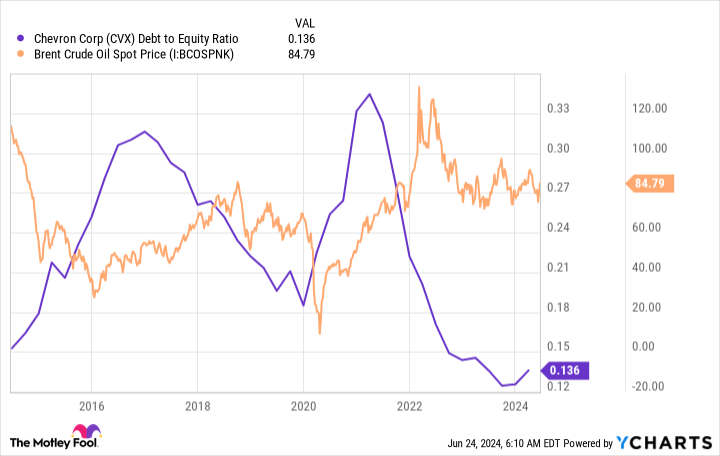

Mainly, when oil costs fall, firms like Chevron are likely to tackle further debt to maintain funding their companies. Within the case of Chevron and Exxon, that money is used to help the dividend. When oil costs enhance, Chevron pays off the debt it took on, so it’s ready for the subsequent business downturn. The chart under reveals this gorgeous clearly.

So, shopping for Chevron at present will go away you proudly owning the strongest firm, financially talking, within the power sector. And it has a extra enticing yield than its closest peer, Exxon. However there’s another issue to think about, and that is the Hess deal. Even when Chevron does not find yourself buying Hess, it’s massive sufficient and financially sturdy sufficient to easily exit and discover one other firm to purchase. In different phrases, the detrimental sentiment right here is basically primarily based on a short-term challenge.

Do not be afraid to purchase this business laggard

On the finish of the day, Chevron is a well-run power firm with a rock-solid monetary basis. Positive, there is a very public detrimental hanging over the inventory proper now, however it will not final without end, and Chevron is greater than able to coping with the issue. For traders who wish to personal an power inventory and that suppose long-term, Chevron might be one of the best place for $1,000 (or extra) at present.

Don’t miss this second probability at a probably profitable alternative

Ever really feel such as you missed the boat in shopping for probably the most profitable shares? Then you definitely’ll wish to hear this.

On uncommon events, our skilled workforce of analysts points a “Double Down” inventory suggestion for firms that they suppose are about to pop. Should you’re frightened you’ve already missed your probability to speculate, now’s one of the best time to purchase earlier than it’s too late. And the numbers converse for themselves:

-

Amazon: when you invested $1,000 once we doubled down in 2010, you’d have $21,765!*

-

Apple: when you invested $1,000 once we doubled down in 2008, you’d have $39,798!*

-

Netflix: when you invested $1,000 once we doubled down in 2004, you’d have $363,957!*

Proper now, we’re issuing “Double Down” alerts for 3 unimaginable firms, and there is probably not one other probability like this anytime quickly.

See 3 “Double Down” shares »

*Inventory Advisor returns as of June 24, 2024

Reuben Gregg Brewer has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Chevron. The Motley Idiot has a disclosure coverage.

The Finest Power Inventory to Make investments $1,000 in Proper Now was initially printed by The Motley Idiot