Stock-Split Stock I Think Is the Best Buy and Hold Over the Next 10 Years.")

It is no secret that semiconductor shares have been notably massive winners amid the bogus intelligence (AI) revolution. With share costs skyrocketing, a number of high-profile chip firms have opted for inventory splits this 12 months. Some AI chip stock-split shares you would possibly acknowledge embrace Nvidia (NASDAQ: NVDA), Tremendous Micro Laptop (NASDAQ: SMCI), and Broadcom (NASDAQ: AVGO).

Certainly, every of those shares has executed wonders for a lot of portfolios during the last couple of years. Nonetheless, I see one in all these chip shares because the superior selection over its friends.

Let’s break down the total image at Nvidia, Supermicro, and Broadcom and decide which AI chip stock-split inventory could possibly be the most effective buy-and-hold alternative for long-term traders.

1. Nvidia

For the final two years, Nvidia has not solely been the largest title within the chip area but additionally basically emerged as the final word gauge of AI demand at giant. The corporate makes a speciality of designing refined chips, often called graphics processing items (GPUs), and information middle companies. Furthermore, Nvidia’s compute unified machine structure (CUDA) supplies a software program element that may used along with its GPUs, offering the corporate with an enviable and profitable end-to-end AI ecosystem.

Whereas all that appears nice, traders can not afford to be starry-eyed as a result of Nvidia’s present dominance. The desk under breaks down Nvidia’s income and free-cash-flow development tendencies during the last a number of quarters.

|

Class |

Q2 2023 |

Q3 2023 |

This autumn 2023 |

Q1 2024 |

Q2 2024 |

|---|---|---|---|---|---|

|

Income |

101% |

206% |

265% |

262% |

122% |

|

Free money movement |

634% |

Not materials |

553% |

473% |

125% |

Knowledge supply: Nvidia Investor Relations.

Admittedly, it is arduous to throw shade on an organization that’s persistently delivering triple-digit income and revenue development. My concern with Nvidia just isn’t associated to the extent of its development however reasonably its tempo.

For the corporate’s second quarter of fiscal 2025 (ended July 28), Nvidia’s income and free money movement rose 122% and 125% 12 months over 12 months, respectively. This can be a notable slowdown from the final a number of quarters. It is truthful to level out that the semiconductor business is cyclical, and an element like that might affect development in any given quarter. Sadly, I believe there’s extra beneath the floor with Nvidia.

Specifically, Nvidia faces rising competitors from direct business forces, akin to Superior Micro Units, and tangential threats from its prospects — specifically, Tesla, Meta, and Amazon. In principle, as competitors within the chip area rises, prospects can have extra choices.

This leaves Nvidia with much less leverage, which is able to doubtless diminish a few of its pricing energy. In the long term, this might take a hefty toll on Nvidia’s income and revenue development. For these causes, traders would possibly need to take into account some alternate options to Nvidia.

2. Tremendous Micro Laptop

Supermicro is an IT structure firm specializing in designing server racks and different infrastructure for information facilities. Lately, hovering demand for semiconductor chips and information middle companies has served as a bellwether for Supermicro. Furthermore, the corporate’s shut alliance with Nvidia has proved notably useful.

That stated, I’ve some issues with Supermicro. As an infrastructure enterprise, the corporate depends closely on different firms’ capital expenditure wants. This makes Supermicro’s development vulnerable to exterior variables, akin to demand for information middle companies, chips, server racks, and extra. Moreover, Supermicro is much from the one IT structure specialist available in the market.

Competitors from Dell, Hewlett Packard, and Lenovo (simply to call a number of) convey their very own ranges of experience to {the marketplace}. On account of competing in such a commoditized environment, Supermicro will be compelled to compete on worth — which takes a toll on revenue technology.

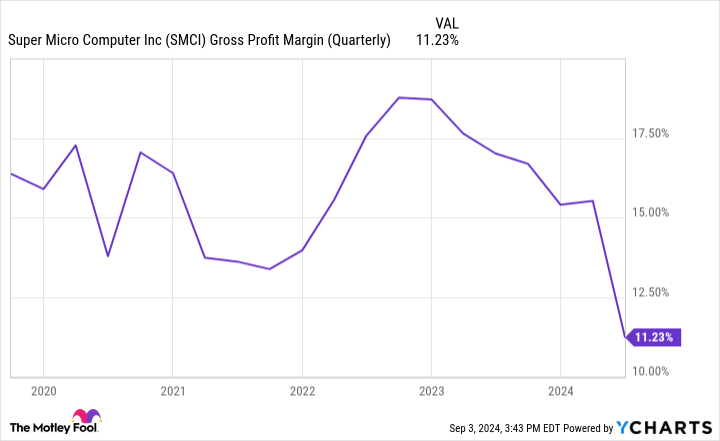

Infrastructure companies don’t carry the identical margin profile as software program firms, as an example. On condition that the corporate’s gross margins are pretty low and in decline, traders should be cautious. Whereas Supermicro’s administration tried to guarantee traders that the margin deterioration is the results of some logjams within the provide chain, more moderen information would possibly sign that gross margin is the least of the corporate’s issues.

Supermicro was lately the goal of a brief report revealed by Hindenburg Analysis. Hindenburg alleges that Supermicro’s accounting practices have some flaws. Following the brief report, Supermicro responded in a press launch outlining that the corporate is delaying its annual submitting for fiscal 12 months 2024.

Given the unpredictability of demand prospects, a fluctuating margin and revenue dynamic, and the allegations surrounding its accounting practices, I believe traders now have higher choices within the chip area.

3. Broadcom

By technique of elimination, it is clear that Broadcom is my prime buy-and-hold selection amongst chip shares proper now. This isn’t as a result of Broadcom’s returns this 12 months have lagged its counterparts, although. The underlying causes Broadcom’s shares have paled in comparison with different chip shares may shine some mild on why I believe its finest days are forward.

I see Broadcom as a extra diversified enterprise than Nvidia and Supermicro. The corporate operates throughout a number of development markets, together with semiconductors and infrastructure software program. Grand View Analysis estimates that the full addressable market for programs infrastructure within the U.S. was valued at $136 billion again in 2021 and was set to develop at a compound annual development fee of 8.4% between 2022 and 2030.

Techniques infrastructure contains alternatives in information facilities, communications, cloud computing, and extra. Contemplating firms of all sizes are more and more counting on digital infrastructure to make data-driven choices, I see the position Broadcom performs in community safety and connectivity as a serious alternative and suppose its latest acquisition of VMware is especially savvy and can assist unlock new development potential.

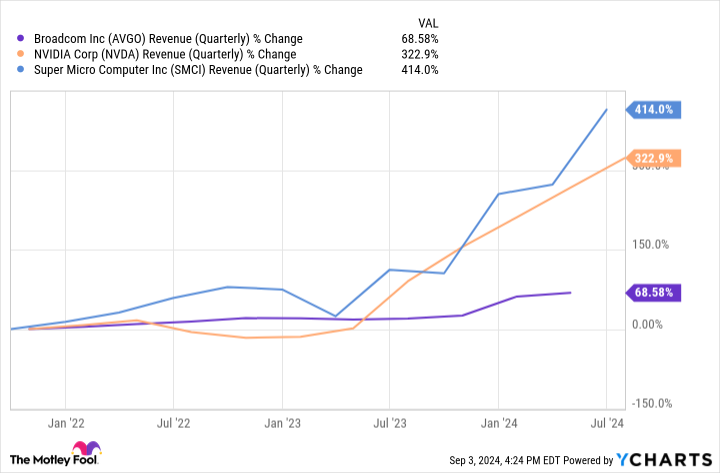

If you happen to have a look at the expansion tendencies within the chart above, it is apparent that Broadcom just isn’t experiencing the identical degree of demand as Nvidia and Supermicro proper now. I believe it’s because Broadcom’s place within the broader AI realm is but to expertise commensurate development in comparison with shopping for chips and storage options in droves.

Whereas I am not saying Nvidia or Supermicro are poor decisions, I believe their futures look cloudier than Broadcom’s proper now. I consider Broadcom is within the very early levels of a brand new development frontier that includes many alternative themes (with AI being simply one in all them). For these causes, I see Broadcom as the best choice explored on this piece and suppose long-term traders have a profitable alternative to scoop up shares and maintain on tight.

Do you have to make investments $1,000 in Broadcom proper now?

Before you purchase inventory in Broadcom, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 finest shares for traders to purchase now… and Broadcom wasn’t one in all them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… in the event you invested $1,000 on the time of our advice, you’d have $630,099!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of September 3, 2024

John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Amazon, Meta Platforms, Nvidia, and Tesla. The Motley Idiot has positions in and recommends Superior Micro Units, Amazon, Meta Platforms, Nvidia, and Tesla. The Motley Idiot recommends Broadcom. The Motley Idiot has a disclosure coverage.

Nvidia, Tremendous Micro, or Broadcom? Meet the Synthetic Intelligence (AI) Inventory-Break up Inventory I Suppose Is the Greatest Purchase and Maintain Over the Subsequent 10 Years. was initially revealed by The Motley Idiot