")

Inventory splits are seeing a renaissance. Over the past 15 years, we have now been within the midst of a raging bull market with minimal interruptions, resulting in large successful shares buying and selling at sky-high costs. To make it simpler to present inventory choices to workers and for small-time traders to purchase shares, corporations have began to implement extra inventory splits. Amazon, Nvidia, and Chipotle are latest inventory break up examples, however there are lots of others on the market.

Buyers have constructed up a story that inventory splits drive worth. There may be an concept that by making a inventory commerce at a cheaper price however with a bigger whole quantity of shares excellent, the inventory is one way or the other cheaper. Does this narrative maintain up in actuality? Let’s check out a inventory break up candidate — Costco (NASDAQ: COST) — to research this phenomenon and whether or not you should purchase forward of a possible inventory break up announcement.

Costco’s upcoming one-comma milestone

Costco inventory is up round 650% within the final 5 years and not too long ago surpassed $900 a share. If it goes up by slightly greater than 10%, it would attain the $1,000 milestone. A real testomony to the sturdy progress of the low-price membership retail mannequin, Costco is now one of many largest corporations in the USA with a market cap of $400 billion.

The inventory has posted a 150,000% whole return since going public over 40 years in the past (whole returns embrace dividend reinvestment), making it one of many best-performing shares ever. For any investor who has held for the reason that early days, a $1,000 funding can be price $1.5 million now.

Alongside the best way, Costco has applied two inventory splits as a result of its rising inventory worth. One in 1993, and one in 2000. With its worth closing in on 4 digits, traders are possible anticipating Costco to implement one other inventory break up someday quickly. When a inventory worth will get over $1,000 a share, administration groups will typically look to separate the inventory to make it extra inexpensive for traders with small sums of cash and to have extra flexibility to present workers smaller slices of inventory as a type of revenue.

Examples of latest inventory splits round $1,000 or greater embrace Chipotle, Nvidia, and Broadcom. If you happen to take a look at its historical past, Costco could also be overdue for a inventory break up proper now.

A thriving enterprise at a premium valuation

Let’s overlook about inventory splits for a second. How is Costco’s enterprise doing? Nicely, simply nice and dandy, thanks for asking. Final quarter that led to Could, income grew 9.1% year-over-year to $57.4 billion. Progress was robust throughout the board however particularly internationally, the place same-store gross sales grew 8.5% year-over-year when adjusted for gasoline costs. E-commerce progress has additionally been strong, up 21% within the quarter.

The worldwide runway for progress seems robust. For instance, a Costco not too long ago opened in Okinawa Japan, and noticed a five-hour wait to enter the door on its first day. Costco has a unbelievable model abroad, even perhaps stronger than the USA the place it competes extra closely with Amazon and Walmart. Administration simply raised costs on its membership charges as nicely. The premium membership now prices $130 a 12 months vs. $120 beforehand.

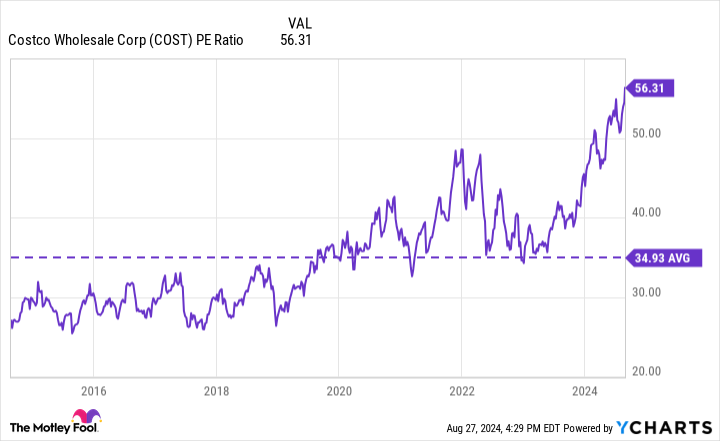

Whereas all that is nice, the inventory trades at fairly a premium valuation. In comparison with its final twelve months earnings, the inventory has a price-to-earnings ratio (P/E) of 56. The inventory’s common over the past 10 years is 35, and this P/E is near an all-time excessive. Bear in mind too that Costco was a a lot smaller firm 10 years in the past.

COST PE Ratio information by YCharts

Does a inventory break up imply you should purchase the inventory?

Let me minimize to the chase: No one besides Costco’s workers (who can get extra versatile choices packages) ought to care a couple of potential inventory break up. For traders immediately, the inventory break up is meaningless, even when it means you should buy the next variety of shares. That is very true when contemplating the rise of fractional buying and selling, the place brokerages mean you can purchase lower than one share at a time when the worth is sky-high like with Costco.

A inventory break up is meaningless as a result of it doesn’t change the underlying enterprise operations. If I offer you a whole pizza and name it “one” piece, is there magically extra pizza after I minimize it into 12 slices? No, and the identical logic applies to a inventory break up. Do not buy Costco for any potential inventory break up, even when one might be forthcoming.

As a substitute, traders ought to concentrate on the enterprise and the inventory’s valuation primarily based on its earnings energy. Costco is a good enterprise, there isn’t any denying that. But it surely trades at an prolonged P/E and can solely develop at a gradual fee over the following 10-20 years as a result of its big income base. Because of this, traders ought to keep away from shopping for the inventory at immediately’s worth.

Must you make investments $1,000 in Costco Wholesale proper now?

Before you purchase inventory in Costco Wholesale, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 finest shares for traders to purchase now… and Costco Wholesale wasn’t certainly one of them. The ten shares that made the minimize may produce monster returns within the coming years.

Think about when Nvidia made this listing on April 15, 2005… for those who invested $1,000 on the time of our suggestion, you’d have $731,449!*

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of August 26, 2024

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Brett Schafer has positions in Amazon. The Motley Idiot has positions in and recommends Amazon, Chipotle Mexican Grill, Costco Wholesale, Nvidia, and Walmart. The Motley Idiot recommends the next choices: brief September 2024 $52 places on Chipotle Mexican Grill. The Motley Idiot has a disclosure coverage.

After Chipotle and Nvidia, Is Costco the Subsequent Huge Inventory-Break up Inventory? (And Ought to You Care?) was initially revealed by The Motley Idiot