Anybody concerned within the investing recreation will understand it’s all about ‘inventory selecting.’ Choosing the proper inventory to place your cash behind is important to make sure sturdy returns on an funding. Subsequently, when the Wall Road professionals take into account a reputation to be a ‘High Choose,’ traders ought to take notice.

Utilizing the TipRanks platform, we’ve appeared up particulars on two shares which have just lately gotten ‘High Choose’ designation from among the Road’s analysts.

So, let’s dive into the small print and discover out what makes them so. Utilizing a mixture of market information, firm stories, and analyst commentary, we will get an thought of simply what makes these shares compelling picks for the remainder of 2023, and why each are rated as Robust Buys by the analyst consensus.

EyePoint Prescribed drugs (EYPT)

We’ll begin within the biotech sector with EyePoint Prescribed drugs, a small-cap biopharma firm working at each the medical and industrial phases. The corporate is actively growing a brand new drug for the therapy of a number of eye circumstances, has one other product in the marketplace, and has just lately bought off a profitable industrial product.

EyePoint has two drug supply platforms, Durasert and Verisome, that permit for injectable, long-term, drug supply. The primary, Durasert, is used with the EYP-1901 drug candidate, a possible therapy for moist age-related macular degeneration (wAMD) and non-proliferative diabetic retinopathy (NPDR). The second platform, Verisome, is used with the commercial-stage product DEXYCU, a drug for the therapy of post-operative irritation after eye surgical procedures. The platforms carry the benefit of dosing on a schedule of months, fairly than days or hours.

A better take a look at EyePoint’s pipeline reveals that the candidate EYP-1901 dominates the corporate’s analysis program. This drug is the topic of two main medical trials: the DAVIO trial, which focuses on the therapy of wAMD, and the PAVIA trial, which targets NPDR. In late March, EyePoint accomplished enrollment within the Section 2 DAVIO trial, which was described as ‘oversubscribed.’ The discharge of topline information is anticipated by the tip of 4Q23. In a current press launch dated June 5, EyePoint introduced the completion of enrollment within the Section 2 PAVIA trial of EYP-1901 for NPDR therapy. The trial aimed to enroll 60 sufferers, however finally enrolled 77. Topline information is anticipated to be launched throughout 2Q24.

On the industrial aspect, the corporate’s present commercial-stage drug is DEXYCU, a one-time injectable therapy for irritation that may happen after ocular surgical procedures. DEXYCU skilled a big decline in product income throughout Q1, which was attributed to the conclusion of the pass-through reimbursement interval on January 1 of this yr. Nonetheless, the corporate is actively engaged in commercialization actions for the drug.

EyePoint additionally reported outcomes for a second industrial product in 1Q23. This product, YUTIQ, accounted for almost all of the corporate’s income, contributing roughly $7.4 million out of a complete of $7.7 million. YUTIQ’s income witnessed a year-over-year enhance of 60%. Following the quarter, EyePoint introduced in Might that it had bought YUTIQ to Alimera Sciences for a complete of $82.5 million in money, together with royalties. The sale allowed EyePoint to retire its excellent financial institution debt and lengthen its money runway till 2025.

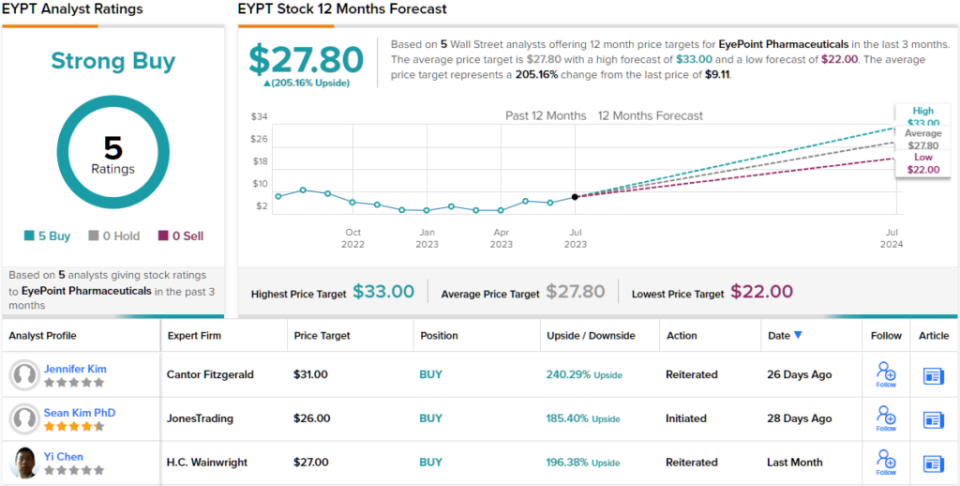

The primary story right here, nevertheless, is all in regards to the analysis pipeline, within the view of Cantor analyst Jennifer Kim. She writes of EyePoint, “We’re calling consideration to EYPT as considered one of our prime picks [for] 2H23. We consider administration’s continued execution and up to date medical & aggressive developments deserve higher consideration forward of key upcoming readouts: 1) Section 2 DAVIO 2 information in moist age-related macular degeneration (wAMD) in December ’23, and a pair of) Section 2 PAVIA information in non-proliferative diabetic retinopathy (NPDR) in 2Q24. We proceed to consider that the height gross sales alternative for EYP-1901 is under-appreciated, and consider the danger/reward is favorable heading into DAVIO 2 information.”

Placing her stance right into a quantifiable mode, Kim charges EYPT shares an Obese (i.e. Purchase) and units her value goal at $31, implying a robust 240% upside for the subsequent 12 months. (To observe Kim’s observe report, click on right here)

Total, the sturdy upside on this inventory has made an impression the Road; all 5 of the current analyst opinions are constructive, for a Robust Purchase consensus score. The inventory’s $9.11 buying and selling value and $27.80 common value goal mix to recommend a 205% one-year upside potential. (See EYPT inventory forecast)

Cogent Biosciences (COGT)

Subsequent up, we’ll take a look at Cogent Biosciences, a precision medication firm centered on the therapy of genetically-driven illnesses. These can embrace autoimmune circumstances and different uncommon illnesses, and even numerous harmful cancers. Sometimes, these circumstances have excessive unmet medical wants. Cogent is engaged on options to enhance the standard of life for sufferers, by concentrating on the genetic mutations behind the illness circumstances.

The corporate’s give attention to the genetic causes of illness is the important thing to its strategy – Cogent seeks to maneuver past simply treating signs, and to impact a remedy. To this finish, the corporate’s drug pipeline options bezuclastinib, a precision medication designed to particularly goal exon 17 mutations when discovered within the KIT receptor tyrosine kinase. The KIT receptor KIT D816V will be locked in an ‘on’ state, inflicting systemic mastocytosis, or AdvSM. This can be a illness situation through which mast cells accumulate within the inside organs. Mutations in exon 17 have additionally been implicated in GIST, gastrointestinal stromal tumors. Bezuclastinib is a potent inhibitor of KIT exercise, and is extremely selective in its exercise. The drug candidate has proven, in early-stage trials, excessive potential within the therapy of exon 17-related circumstances.

Cogent is presently conducting a number of medical trials of bezuclastinib, with specific give attention to the 2 most superior trials. The primary trial is the Section 2 APEX trial for the therapy of AdvSM. Half 1 of the continuing Section 2 trial accomplished enrollment, and Half 2 has commenced enrollment in April with a goal of 65 sufferers. The corporate anticipates releasing information from 30 sufferers in Half 1 of the APEX trial through the second half of 2023.

The second superior medical trial is the Section 3 PEAK trial within the therapy of GIST. Knowledge launched in June confirmed a 55% illness management charge in closely pre-treated GIST sufferers, and confirmed that bezuclastinib together with sunitinib was well-tolerated with an appropriate security profile. The corporate is now actively enrolling sufferers in Half 2 of the PEAK trial, and additional information is anticipated to be launched in 2H23.

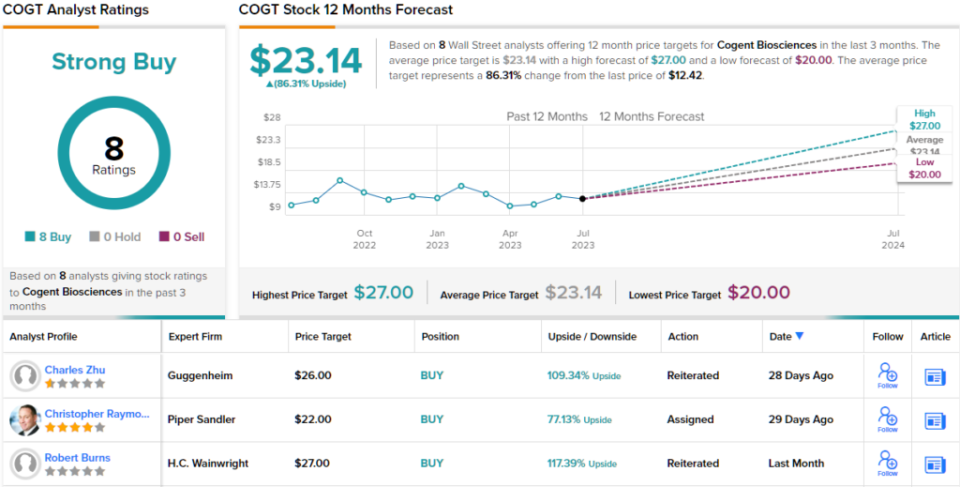

Piper Sandler analyst Christopher Raymond is impressed by bezuclastinib, notably by the APEX and PEAK trials. In assist of designating this inventory as a ‘High Choose,’ Raymond confidently states, “Our thesis on this identify is that bezuclastinib’s distinctive mutational selectivity and security profile place it nicely throughout the SM illness spectrum. With early AdvSM information that stacks up favorably to avapritinib, we’re assured that updates later this yr in each AdvSM and ISM will proceed to assist bezuclastinib’s best-in-class potential. In GIST, whereas the ASCO replace was early, we expect the thesis is enjoying out precisely as hoped, with indications of a significant medical advance as a mixture remedy with sunitinib in 2L GIST. We stay consumers of this identify in entrance of numerous derisking information occasions this later yr.”

Unsurprisingly, Raymond charges Cogent an Obese (i.e. Purchase), whereas his $22 value goal on the shares implies a 77% upside potential on the one-year horizon. (To observe Raymond’s observe report, click on right here)

Total, there are 8 current analyst opinions on this inventory and all are constructive, for a unanimous Robust Purchase consensus. The shares are promoting for $12.42 and the typical value goal of $23.14 implies an 86% acquire within the subsequent 12 months. (See COGT inventory forecast)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely essential to do your personal evaluation earlier than making any funding.