Stock. You Could Follow Her Lead for Less Than $20 per Share.")

In the case of synthetic intelligence (AI), the “Magnificent Seven” shares in all probability come to thoughts. The moniker contains the vast majority of megacap firms main the AI revolution: Apple, Alphabet, Microsoft, Nvidia, Tesla, Meta Platforms, and Amazon.

One firm that could be getting missed within the AI arms race is Palantir (NYSE: PLTR). Whereas the info analytics firm is finest recognized for its shut ties to the U.S. army and its allies, Palantir is excess of a authorities contractor. It has a rising presence within the personal sector and works with clients throughout a wide range of markets.

But regardless of this, the inventory is buying and selling roughly 50% beneath its all-time highs. And whereas some on Wall Road stay skeptical of Palantir’s long-term potential, one notable investor particularly has been shopping for the dip. The funds of ARK Make investments CEO Cathie Wooden have ratcheted up their shopping for of Palantir as of late.

For the buying and selling interval between Dec. 6 and Dec. 15, Ark funds bought 1.7 million shares in Palantir inventory throughout three exchange-traded funds (ETFs). Whereas the corporate represents only one.2% of Ark’s mixed portfolio, it has an even bigger place than many of the Magnificent Seven shares.

With the inventory buying and selling for simply $18 per share as of this writing, now’s a terrific time to evaluate Palantir’s prospects.

What is going on on?

A current bearish analyst report from funding financial institution William Blair spurred a sell-off in Palantir inventory that wiped practically $4 billion off its market capitalization.

William Blair analyst Louie DiPalma expressed issues a couple of contract that Palantir has with the U.S. Military, suggesting that the upcoming renewal of that contract could also be for lower than the unique deal’s worth. As of this morning, Dec. 15, Palantir helped curtail these worries because the Military contract renewed for a further 12 months. Whereas the preliminary deal was a multiyear contract, long-term buyers should not get hung up on the extension being for just one 12 months. Moderately, there are a number of the explanation why buyers ought to imagine the sell-off was overblown and may very well be a shopping for alternative.

Demand for AI-powered companies is off the charts

It is vital to needless to say the Military contract is only one deal. The developments Palantir has made in synthetic intelligence have led to a surge in demand for its companies that I believe is being missed. Earlier this 12 months, it launched a brand new product referred to as the Palantir Synthetic Intelligence Platform (AIP), which makes use of generative AI and huge language fashions (LLMs) to assist clear up advanced operational challenges.

Whereas this may occasionally sound just like the options supplied by among the large tech giants, Palantir could have an edge because of its artistic lead technology technique. The corporate has been internet hosting immersive seminars it calls “boot camps,” at which potential clients can take a look at out its software program platforms. The purpose of those occasions is to shortly establish use circumstances for its companies, giving Palantir a possibility to promote merchandise and increase gross sales to clients as time goes on.

Whereas the boot camps are nonetheless a brand new innovation for the corporate, demand to attend them is off the charts. Throughout Palantir’s third-quarter earnings name, Chief Technoloyg Officer Shyam Sankar mentioned, “we’re working extra boot camps monthly than we had U.S. business pilots all final 12 months.” The corporate had performed boot camps for 200 organizations by way of November.

These boot camps characterize a means for Palantir to doubtlessly seize a bit of the rising AI marketplace for little value, and maybe shorten its gross sales cycle considerably. As firms attend the seminars and convert into paying clients, Palantir has a possibility to cross-sell and upsell merchandise at a sooner charge. In idea, this could assist it speed up its income development whereas preserving its spending on gross sales, advertising and marketing, and buyer retention low.

Is Palantir’s valuation justified?

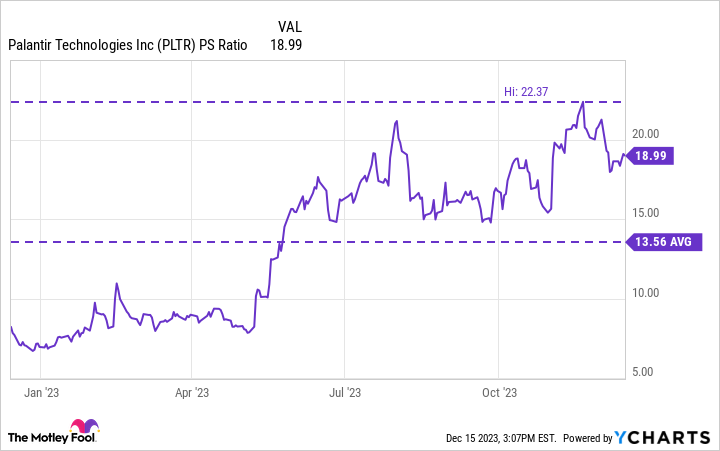

The chart beneath reveals that Palantir’s price-to-sales (P/S) ratio of 19 is at the moment effectively above its one-year common and inching towards prior highs. Whereas this may occasionally appear a bit of wealthy, I see Palantir as deserving of a premium.

In contrast to a lot of its software-as-a-service (SaaS) cohorts, Palantir is already worthwhile on a GAAP (typically accepted accounting rules) foundation. Actually, given its constant income, Palantir is eligible for inclusion within the S&P 500, an enormous milestone for any firm. The factor long-term buyers ought to be contemplating right here is the tempo at which Palantir’s choices are being adopted and deployed.

As an example, throughout Q3 Palantir practically tripled its AIP customers. In accordance with administration, since its launch 5 months in the past, 300 distinctive organizations have deployed AIP. Whereas it is clear that the boot camps are driving curiosity in Palantir’s merchandise, buyers ought to needless to say these prospects are contributing little to no income for Palantir at the moment. Moderately, it is the rising curiosity in attending and testing out AIP that might function a proxy of what Palantir’s future may appear to be. It is these long-term secular tailwinds that appeal to buyers like Wooden, and underscore her conviction to purchase when the inventory falls off a cliff.

In the long term, Palantir’s capability to speed up income development whereas additionally sustaining income appears achievable. Because the inventory experiences some pronounced promoting exercise, now appears like an unbelievable alternative to start dollar-cost averaging right into a long-term place for this AI disrupter.

Must you make investments $1,000 in Palantir Applied sciences proper now?

Before you purchase inventory in Palantir Applied sciences, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they imagine are the 10 finest shares for buyers to purchase now… and Palantir Applied sciences wasn’t one in all them. The ten shares that made the reduce may produce monster returns within the coming years.

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

See the ten shares

*Inventory Advisor returns as of December 11, 2023

Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market growth and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Palantir Applied sciences, and Tesla. The Motley Idiot has positions in and recommends Alphabet, Amazon, Apple, Datadog, Meta Platforms, Microsoft, MongoDB, Nvidia, Palantir Applied sciences, ServiceNow, Snowflake, and Tesla. The Motley Idiot has a disclosure coverage.

Cathie Wooden Simply Made a Huge Buy of This Synthetic Intelligence (AI) Inventory. You May Comply with Her Lead for Much less Than $20 per Share. was initially printed by The Motley Idiot