India’s bank card economic system, an emblem of rising client confidence and digital empowerment, is displaying some indicators of pressure. Bank card delinquencies within the 91–360 days overdue class have soared by a staggering 44.34 per cent over the previous yr, reaching Rs 33,886.5 crore as of March 2025, up from Rs 23,475.6 crore in March 2024, in accordance with the most recent information from CRIF Excessive Mark.

This sharp rise highlights a rising vulnerability amongst debtors, notably within the 91–360 days class, a phase that banking laws categorise as non-performing property (NPAs) within the case of financial institution loans. Successfully, bank card holders have defaulted on almost Rs 34,000 crore of debt that has remained unpaid for over 91 days.

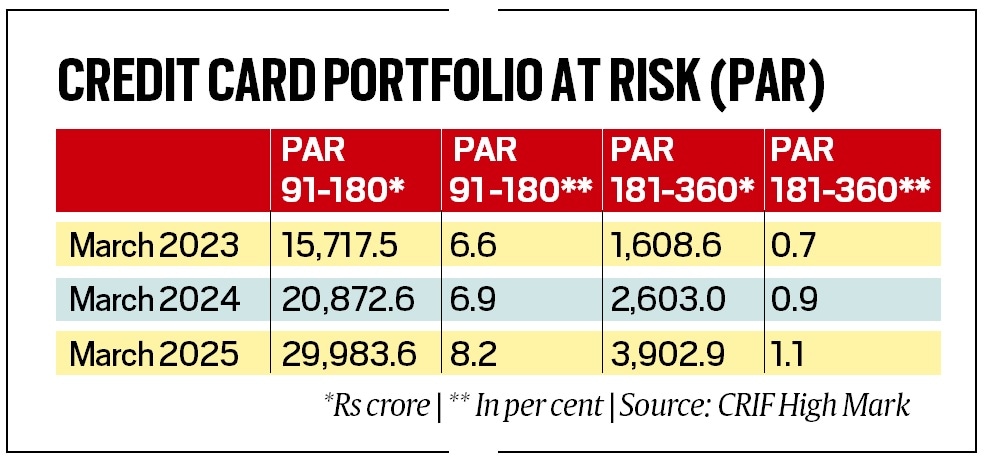

The breakdown of misery

A more in-depth have a look at the numbers reveals a disturbing pattern. Within the 91–180 days overdue phase alone, the delinquent quantity jumped to Rs 29,983.6 crore, in comparison with Rs 20,872.6 crore a yr earlier, and has virtually doubled from the March 2023 degree, information ready by CRIF Excessive Mark for The Indian Categorical says. This displays not only a rising reliance on credit score however a mounting incapacity — or unwillingness — to repay on time.

CRIF Excessive Mark, a credit score bureau registered with the Reserve Financial institution of India (RBI), famous a gentle uptick within the share of portfolio in danger (PAR), which tracks overdue funds. In March 2025, PAR within the 91–180 day bucket reached 8.2 per cent, rising from 6.9 per cent in March 2024 and 6.6 per cent in March 2023 — a constant three-year climb. For loans overdue 181–360 days, the PAR rose to 1.1 per cent, up from 0.9 per cent in 2024 and 0.7 per cent in 2023.

These traits sign each short-term and long-term stress within the unsecured credit score market, particularly as shoppers lean closely on plastic for on a regular basis and discretionary spending. Bank card excellent was Rs 2.90 lakh crore as of Could 2025 as in opposition to Rs 2.67 lakh crore in Could 2024, in accordance with the RBI.

A credit-driven consumption increase

The rise in delinquencies is about in opposition to the backdrop of an explosive rise in bank card utilization throughout the nation. The worth of bank card transactions reached Rs 21.09 lakh crore by March 2025, surging from Rs 18.31 lakh crore the earlier yr — a virtually 15 per cent leap.

This increase mirrors India’s post-pandemic financial restoration and displays rising client confidence. Bank card spending in Could 2025 alone was Rs 1.89 lakh crore, up dramatically from Rs 64,737 crore in January 2021.

Story continues under this advert

Likewise, the variety of bank cards in circulation has ballooned. As of Could 2025, 11.11 crore bank cards have been lively in India, in comparison with 10.33 crore in Could 2024 and simply 6.10 crore in January 2021, in accordance with RBI information.

Folks are likely to borrow and spend extra after they’re optimistic about their monetary future, however might also depend on bank cards to keep up their way of life when wages stagnate or costs rise, stated an funding analyst.

Rewards, presents — and debt traps

What’s fuelling this sharp uptick in utilization? Banks and fintech companies have aggressively promoted bank card adoption with enticing incentives: cashback rewards, journey perks, interest-free EMIs, and airport lounge entry. For a lot of shoppers, particularly in city and upwardly cellular segments, bank cards have turn into synonymous with comfort and way of life.

However the ease of swiping has include a hidden price. Bank card debt is among the many most costly types of borrowing in India. Banks sometimes cost between 42 per cent and 46 per cent annual curiosity on unpaid balances past the interest-free interval.

Story continues under this advert

“Clients usually get lured by flashy presents and rewards. But when they don’t repay on time, they find yourself paying exorbitant curiosity,” stated a senior financial institution official. A number of missed funds can rapidly spiral right into a debt entice.”

Why it issues

The sharp enhance in delinquencies poses a threat not simply to particular person debtors but additionally to the broader monetary system. Bank card loans are unsecured, that means they aren’t backed by collateral. Rising defaults can have an effect on banks’ stability sheets and immediate tighter lending norms, thereby slowing credit score development, a key driver of consumption in India. The RBI certainly hiked the chance weight on bank card excellent in 2023.

Furthermore, defaults have an effect on credit score scores. For people who fall behind on funds, the monetary affect is rapid and long-lasting. A broken credit score rating or historical past can restrict future entry to loans, bank cards, and even rental agreements and job alternatives in some sectors.

Whereas bank cards supply flexibility and monetary freedom, their misuse or overuse can have critical penalties. As extra Indians embrace digital credit score, the main focus should now shift from spending to managing debt responsibly, specialists say.

Story continues under this advert

Banks, regulators and fintechs have to step up instructional initiatives round rates of interest, billing cycles, and compensation self-discipline. For shoppers, the message is obvious: bank cards are a device — not free cash. Use them properly, or threat paying a heavy value.