Whereas electrical automobiles (EVs) are getting the headlines within the automotive business, there are two different tendencies that may reward nearer investor consideration. These are driver help and autonomous automobiles. These are primarily based on comparable applied sciences – superior sensor techniques, machine studying and AI, and interactive interfaces for the human operator – however they fill completely different roles. For buyers, nevertheless, these applied sciences will supply a realm of alternatives the place the rubber meets the highway.

The auto business consultants from funding agency Goldman Sachs have been proper on high of those new developments within the automotive world, and have been significantly obsessed with LiDAR techniques. These are high-tech sensor techniques (the time period is derived from ‘gentle detection and ranging’) utilizing lasers to offer the best attainable precision in vary and velocity details about surrounding objects. LiDAR represents the most recent in sensing tech, and Goldman analyst Allen Chang writes of it, “We consider we’re within the early phases of LiDAR mass adoption and mannequin international assisted driving penetration to rise 3-fold over the following 10 years. This represents among the many quickest development profiles within the EV provide chain over the following decade.”

We are able to comply with the Goldman Sachs lead and use the TipRanks platform to drag up the main points on two of the agency’s LiDAR picks, corporations that the G-S analysts see on the forefront of the LiDAR revolution. Every of those goal corporations has a Sturdy Purchase mixture score from the Wall Road analysts, and Goldman sees them with no less than 80% upside for the approaching 12 months. Let’s check out their particulars, as wells because the Goldman commentaries.

Hesai Group (HSAI)

We’ll begin with Shanghai-based Hesai Group, a world chief within the growth and utility of LiDAR techniques. The corporate’s sensor tech has discovered makes use of in autonomous mobility, after all, but additionally within the trucking business, robotics, and even manufacturing unit manufacturing. As of December 31, 2022, Hesai Group had shipped out over 100,000 LiDAR models, and the corporate has additionally constructed up robust connections with main OEMs within the automotive business, and has a 60% market share within the autonomous mobility – self-driving automotive – area of interest.

Hesai Group solely just lately joined the U.S. public markets, having carried out an preliminary public providing of American Depositary Shares (ADS). The IPO, which closed on February 13, noticed the corporate put 10 million ADSs available on the market at a gap worth of $19 every and lift $190 million in gross proceeds. The IPO was the biggest preliminary providing of a Chinese language inventory on the US markets since 2021.

Final week, simply over a month from the IPO, Hesai launched its first quarterly monetary outcomes as a publicly traded entity on the US NASDAQ alternate. The report, for 4Q22, confirmed a quarterly high line of $59.3 million, for a 56% year-over-year improve. This was supported by a large 739% y/y improve in quarterly LiDAR deliveries which hit 47,515. Of that complete, 43,351 had been ADAS (superior driver help techniques) and 4,164 had been autonomous mobility. Regardless of these successes, Hesai’s inventory has suffered out there downturn and is down 42% since buying and selling started.

Goldman’s Allen Chang, nevertheless, sees sufficient cause to again Hesai. Explaining his bullish stance, he writes, “We spotlight Hesai’s three key aggressive benefits: (1) Know-how – Hesai pursues a novel “ASIC” know-how that integrates key parts to scale back energy consumption, simplify manufacturing and decrease unit value; (2) Manufacturing – Hesai owns a world-class LiDAR manufacturing facility in Shanghai. Their manufacturing and product design reinforce one another, permitting quicker product iteration. (3) Massive home market – China leads ADAS and autonomous adoption, with penetration in new automotive gross sales to develop 10X from 8% to 84% (2021-30E). This enlargement offers the chance for Hesai to scale up its know-how.”

Taking this ahead, Chang sees match to charge the shares as a Purchase, with a $29 worth goal that suggests a strong 123% upside potential for the approaching 12 months. (To observe Chang’s observe file, click on right here.)

In its brief time on the US public markets, Hesai has picked up 3 analyst suggestions – and they’re all optimistic, for a unanimous Sturdy Purchase consensus score. The inventory has a present buying and selling worth of $13.00, and its $28.50 common worth goal suggests a 12-month acquire of 119%. (See Hesai’s inventory forecast at TipRanks.)

Innoviz Applied sciences (INVZ)

Subsequent on our record is Innoviz Applied sciences, one other chief within the world-wide LiDAR market. Innoviz each designs and manufactures high-end solid-state LiDAR sensors, together with the software program required to attach the sensor {hardware} with the controlling laptop techniques. Innoviz has been working with a number of big-name automotive corporations, together with BMW and Volkswagen.

Innoviz shares confirmed a peak in February of this 12 months, and are down 33% from that degree; over the previous two years, the inventory has fallen 65%. Throughout this time, the corporate has been working web losses, and revenues have didn’t take off. A have a look at the corporate’s final monetary report reveals that the complete 12 months 2022 numbers are modestly increased year-over-year, that the 4Q22 missed expectations, and the ahead steering upset.

On the quarterly degree, the corporate confirmed revenues of $1.58 million, lacking the estimates and down nearly 5% year-over-year. The corporate’s This autumn EPS, a 25-cent loss, got here in under the 24-cent loss forecast. Within the full 12 months numbers, the highest line did develop 10% to six million, and the corporate bought a file variety of LiDAR models.

Additional souring sentiment, Innoviz missed on the ahead income steering. The corporate projected complete 2023 revenues in a variety between $12 million and $15 million; whereas this might characterize a doubling – or extra – of the highest line y/y, the analyst consensus had anticipated steering of ~$30 million.

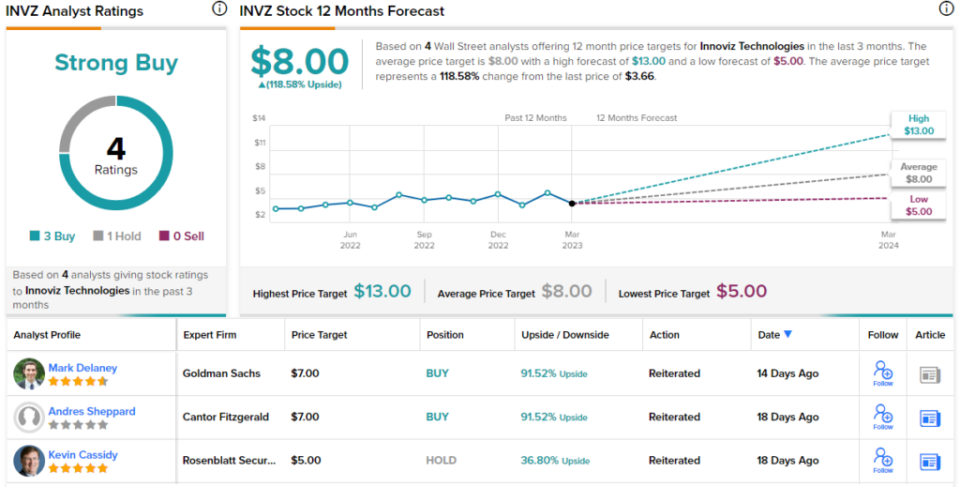

This inventory is roofed for Goldman by 5-star analyst Mark Delaney, who acknowledges the headwinds that the corporate is going through however goes on to stipulate an upbeat prospect: “We consider the 4Q report was an incremental adverse, though we preserve our Purchase score on the inventory reflecting our optimistic view of the corporate’s long-term alternative. Particularly, we consider that the corporate’s order e book stays robust together with design wins at 3 auto OEMs (i.e. BMW, VW, and an Asian primarily based OEM). Whereas the manufacturing ramp up is happening extra slowly than we’d anticipated with 2023 income steering under the Road, we consider that as OEM ADAS applications ramp within the coming years that the corporate will see improved outcomes.”

Quantifying his stance, Delaney charges INVZ shares as a Purchase, and his worth goal, set at $7, signifies his confidence in an upside of 91% for 2023. (To observe Delaney’s observe file, click on right here.)

General, Innoviz has a Sturdy Purchase consensus score from the Road, primarily based on 4 analyst critiques with a 3 to 1 breakdown favoring Purchase over Maintain. The inventory has an $8 common worth goal, increased than the Goldman outlook and suggesting a 118% upside from the buying and selling worth of $3.66. (See Innoviz’s inventory forecast at TipRanks.)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally vital to do your individual evaluation earlier than making any funding.