Goran Babic | E+ | Getty Pictures

Constructing a $1 million nest egg could appear an unattainable feat.

Nevertheless, amassing such retirement wealth is inside attain for nearly anybody — supplied they take sure steps, monetary advisors say.

“You may suppose that, ‘Nicely, I’ve to develop into a Silicon Valley entrepreneur to develop into wealthy,'” mentioned Brad Klontz, a monetary psychologist and licensed monetary planner.

In truth, you generally is a fast-food employee your complete life and amass wealth, mentioned Klontz, a member of the CNBC Monetary Advisor Council and the CNBC International Monetary Wellness Advisory Board.

The calculus is straightforward, he mentioned.

Each time you are paid a greenback, save and make investments a proportion towards your “monetary freedom,” Klontz mentioned.

With this mindset, “you’ll be able to work virtually any job and retire a millionaire,” he mentioned.

It isn’t essentially a ‘Herculean activity’

Saving $1 million might sound like a “Herculean activity” but it surely “won’t be as laborious as you suppose,” Karen Wallace, a CFP and former director of investor schooling at Morningstar, wrote in 2021.

The bottom line is to begin saving early, maybe in a 401(okay) plan, particular person retirement account or taxable brokerage account, specialists mentioned. This permits traders to harness the magic of compound curiosity over many years. In different phrases, you “let your investments do as a lot heavy lifting as attainable,” Wallace wrote.

About 79% of American millionaires say their internet value was “self-made,” based on a Northwestern Mutual ballot printed in September. Simply 11% mentioned they inherited their wealth, whereas 6% obtained it from a windfall occasion like profitable the lottery, based on the survey of 4,588 U.S. adults, fielded from Jan. 3 to Jan. 17, 2024.

Extra from Private Finance:

IRS: There is a key deadline approaching for RMDs

Egg costs might quickly ‘flirt with document highs’

Federal Reserve is more likely to reduce rates of interest subsequent week

There have been 544,000 People with 401(okay) balances of greater than $1 million as of Sept. 30, based on Constancy Investments, which is the most important administrator of office retirement plans. There have been additionally greater than 418,000 IRA millionaires.

In truth, the variety of 401(okay) millionaires grew by 9.5%, or 47,000 folks, between the second and third quarter of 2024, largely because of stock-market features.

How you can get to $1 million

Wera Rodsawang | Second | Getty Pictures

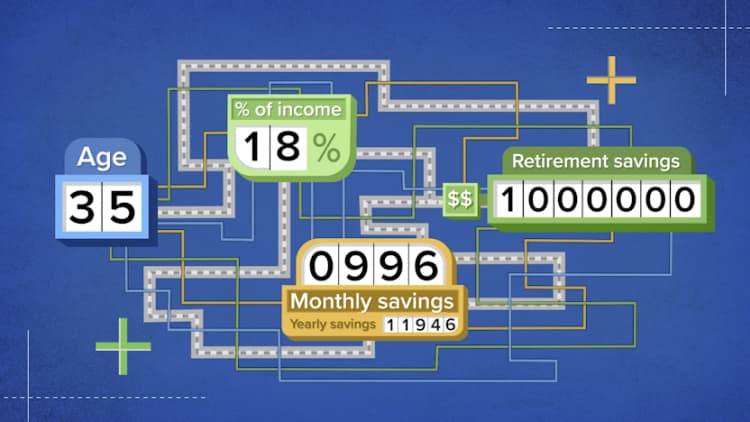

Winnie Solar, a monetary advisor, gives an instance of the maths that hyperlinks $1 million of wealth with constant saving.

For instance a 30-year-old makes $60,000 a yr after tax. In the event that they have been to save lots of $500 a month — or, 10% of their annual earnings — they’d have $1 million by age 70, assuming common market returns of seven%, she mentioned.

This does not account for monetary components that may enhance financial savings over that interval, like an organization 401(okay) match, bonuses or raises.

You’ll be able to work virtually any job and retire a millionaire.

Brad Klontz

monetary psychologist and licensed monetary planner

“In 40 years, you may have over $1 million, and that is doing nothing else however $500 a month,” mentioned Solar, co-founder of Solar Group Wealth Companions, based mostly in Irvine, California, and a member of CNBC’s Monetary Advisor Council.

It is also necessary to keep away from debt, which might be the “largest cavity” for constructing financial savings, and check out to not improve bills an excessive amount of, Solar defined.

Timing is extra necessary than being excellent, Solar mentioned.

She recommends beginning with a low-cost index fund — like one monitoring the S&P 500, which diversifies financial savings throughout the most important publicly traded U.S. firms — and constructing from there.

“Even ready a yr could make a dramatic distinction in reaching that $1 million level,” Solar mentioned. “Cease and take motion.”

What’s the correct amount of financial savings?

Damircudic | E+ | Getty Pictures

In fact, $1 million in retirement might not be the correct amount for everybody.

An oft-cited rule of thumb — referred to as the 4% rule — signifies a typical retiree can draw about $40,000 a yr from a $1 million nest egg to be able to safely assume they will not run out of cash in retirement. (That annual withdrawal is adjusted yearly for inflation.)

For a lot of, this sum can be supplemented by Social Safety.

Constancy suggests a financial savings aim based mostly on earnings. For instance, by age 67 a employee ought to purpose to have saved 10 instances their annual wage to make sure for a snug retirement.

Ideally, households would purpose to save lots of 15% to twenty% of their earnings, Solar mentioned. This can be a rule of thumb typically cited by monetary planners.

How a lot wealth you need — and the way shortly you need to be wealthy — will decide the proportion, Klontz mentioned.

He is personally aimed for a 30% financial savings price, however is aware of individuals who’ve shot for near 90%. Saving such massive chunks of 1’s earnings is a standard thread of the so-called FIRE motion, which stands for Monetary Independence, Retire Early.

How do they do it?

“They did not transfer out of their dad and mom’ home, they minimized every little thing, they do not purchase new garments, they take the bus, they shave their head as a substitute of paying for haircuts,” Klontz mentioned. “There’s all types of hacks you are able to do if you wish to get there sooner.”

How you can get pleasure from immediately and save for tomorrow

In fact, there is a stress right here for individuals who need to get pleasure from life immediately and save for tomorrow.

“We weren’t meant to solely survive and get monetary savings,” Solar mentioned. “There needs to be that good high quality of life and that glad medium.”

One technique is to allocate 20% of family bills towards the factor or issues which are most necessary to you — maybe huge holidays, fancy automobiles, or the latest expertise, Solar mentioned.

Make some concessions — i.e., “scrimp and save” — on the opposite 80% of family prices, she mentioned. This helps savers really feel like they don’t seem to be lowering their high quality of life, she mentioned.