During the last 12 months, traders have turned to the “Magnificent Seven” shares seeking outsized positive aspects, and for good cause.

Mega-cap tech firms resembling Nvidia, Microsoft, Alphabet, and Meta Platforms have all outperformed the S&P 500 and Nasdaq Composite during the last 12 months. A lot of those positive aspects might be attributed to a rising curiosity in synthetic intelligence (AI), a market dominated by the Magnificent Seven.

But regardless of the spectacular performances of the businesses above, I see one other member of the Magnificent Seven as a superior alternative for long-term traders.

E-commerce and cloud computing big Amazon (NASDAQ: AMZN) has underperformed the Nasdaq during the last 12 months and has mainly generated returns consistent with these of the S&P 500.

With shares down roughly 14% during the last month, I believe now could be a main alternative to purchase the dip in Amazon.

Let’s dig into how Amazon is quietly disrupting the AI panorama and assess why now seems to be like a profitable alternative to scoop up shares at a dirt-cheap valuation.

Do not name it a comeback

One of many greatest alternatives surrounding AI is cloud computing. Amazon faces fierce competitors within the cloud infrastructure market from Microsoft Azure and Alphabet’s Google Cloud Platform (GCP).

During the last 18 months or so, Microsoft has swiftly augmented the Azure platform due to the corporate’s $10 billion funding in OpenAI — the developer of ChatGPT. Furthermore, Alphabet has achieved a good job of breaking into the cloud realm due to a sequence of acquisitions, together with MobiledgeX, Forseeti, Siemplify, and Mandiant.

These strikes by Microsoft and Alphabet initially seemed to be taking a toll on Amazon’s cloud income development and its profitability. Nevertheless, the desk under illustrates some newfound encouraging tendencies from Amazon’s cloud phase, Amazon Internet Companies (AWS).

|

Class |

Q1 2023 |

Q2 2023 |

Q3 2023 |

This autumn 2023 |

Q1 2024 |

Q2 2024 |

|---|---|---|---|---|---|---|

|

AWS Income Yr over Yr % Development |

16% |

12% |

12% |

13% |

17% |

19% |

|

AWS Working Revenue Yr over Yr % Development |

(26%) |

(8%) |

30% |

39% |

83% |

72% |

Knowledge supply: Investor Relations

The figures above showcase a very optimistic narrative for Amazon. During the last 12 months, AWS has transitioned from a enterprise experiencing constant deceleration to 1 that has now grown in three consecutive quarters, all whereas considerably growing working revenue.

Amazon is a money-printing machine

Seeing a return to income and revenue development is good to see, but it surely’s just one a part of the higher story for Amazon.

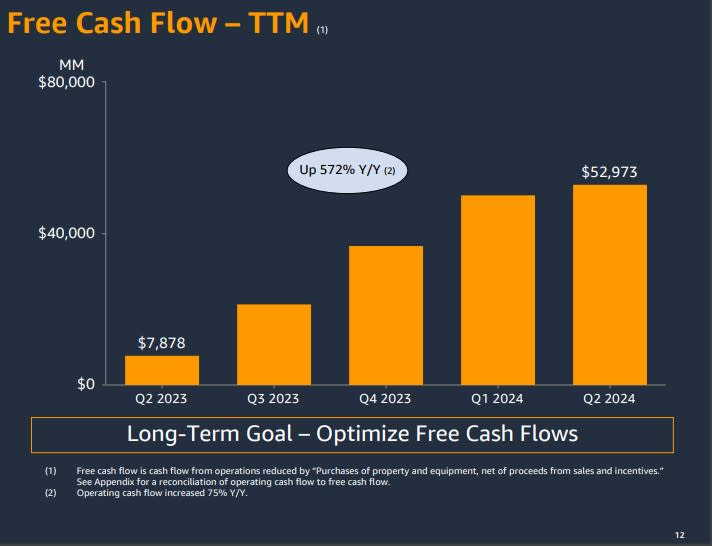

Nearly all of Amazon’s working income stem from AWS. Because of this, the reacceleration of the cloud enterprise has instantly impacted Amazon’s general money movement profile. For the quarter ended June 30, Amazon generated $53 billion of free money movement on a trailing-12-month foundation. Moreover, with a stability sheet boasting $86 billion of money and equivalents, Amazon has nearly no scarcity to speculate aggressively and provides its rivals a run for his or her cash.

One of many catalysts sparking renewed development in AWS is Amazon’s $4 billion funding in generative AI start-up Anthropic.

This relationship is especially vital as a result of Anthropic is coaching its AI fashions on Amazon’s in-house semiconductor chips — Trainium and Inferentia. This supplies Amazon with a direct line to compete in opposition to Nvidia as demand for semiconductor chips continues to growth.

Furthermore, the corporate can also be investing $11 billion into an information heart undertaking in Indiana. To me, these investments solidify Amazon’s ambitions to compete all throughout the AI panorama as AWS enters a brand new part of its evolution.

For these causes, I believe the income development and renewed income from AWS, as proven above, are solely the start.

A main valuation for traders

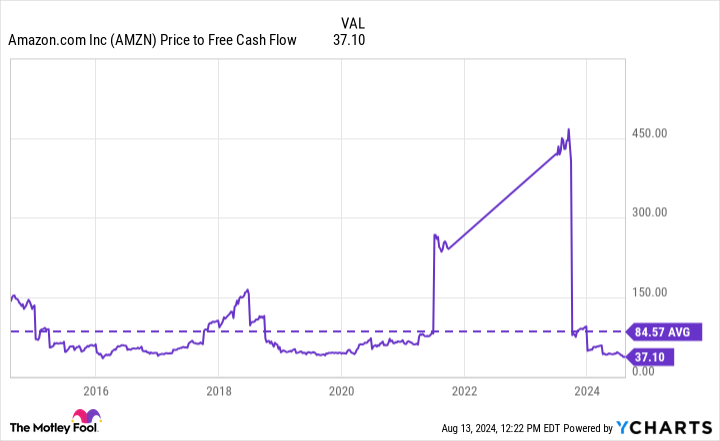

Amazon at present trades at a price-to-free-cash-flow (P/FCF) a number of of 37.1, which is lower than half its 10-year common. I discover this peculiar, contemplating that Amazon is a a lot bigger and much more subtle enterprise at the moment than it was a decade in the past.

To me, traders are both overlooking or unappreciative of Amazon’s dive into the AI realm. I believe AI’s future potential could also be baked into a few of Amazon’s Magnificent Seven compatriots, provided that lots of them have handily outperformed the markets during the last 12 months.

In contrast, Amazon is already reaping the rewards from these AI-driven initiatives, and the corporate has a boatload of money to maintain funding the expansion for fairly a while. For these causes, I believe Amazon is essentially the most profitable alternative amongst mega-cap tech shares proper now. In my eyes, this is a wonderful alternative to purchase Amazon inventory hand over fist.

Must you make investments $1,000 in Amazon proper now?

Before you purchase inventory in Amazon, think about this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they imagine are the 10 greatest shares for traders to purchase now… and Amazon wasn’t one in every of them. The ten shares that made the lower might produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… when you invested $1,000 on the time of our advice, you’d have $763,374!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of August 12, 2024

Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market growth and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Idiot has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

If I May Solely Make investments In 1 “Magnificent Seven” Inventory Over the Subsequent Decade, This Would Be It was initially printed by The Motley Idiot