Stock Looks Cheaper than NVDA & AMD on a Forward Basis, but I’m Cautious")

Intel (INTC) has discovered itself in a world of bother in 2024 after years of innovation failures left it considerably lagging behind its friends. So much has occurred in current months, and there are numerous extra developments doable earlier than the top of the yr. Curiously, analysts nonetheless see the enterprise recovering to the extent that the inventory turns into fairly reasonably priced in comparison with friends in upcoming years. Regardless of this, I’m involved the corporate will battle to catch up, and as such, I’m impartial on INTC.

What Occurred at Intel?

Intel stays a world chip large, with operations in each the design and manufacturing of chipsets. Nevertheless, the decline from its once-dominant place within the semiconductor trade is obvious, and may be attributed to quite a lot of components which have unfolded over the previous decade. These pressures proceed, and so I’ve a impartial ranking on the inventory.

The corporate’s battle to take care of its technological edge started round 2015 when it merely stopped innovating as rapidly as its friends. Because the innovation cycles didn’t ship materials enhancements and different firms transitioned to smaller, extra environment friendly chip manufacturing processes, Intel continued making income because it produced its much less superior chips en masse.

This lack of innovation finally caught up with Intel. The corporate’s reliance on its x86 structure additionally left it susceptible because the trade shifted in direction of extra energy-efficient ARM-based (ARM) designs, significantly in cell and rising synthetic intelligence (AI) purposes. Intel’s weaknesses have been laid naked through the pandemic as provide chain disruptions and elevated demand for computing energy highlighted the corporate’s manufacturing limitations.

Intel’s Catch-Up Technique

In response to falling behind, Intel introduced in CEO Pat Gelsinger in 2021 to spearhead a turnaround technique, which included huge investments in new fabrication services and a renewed concentrate on technological management.

Gelsinger kicked issues off by asserting his formidable “5 nodes in 4 years” technique, with the purpose of rebounding as rapidly as doable. Nevertheless, the highway to restoration has been difficult, with Intel dealing with intense competitors and a troublesome climb to regain buyer confidence in its potential to ship cutting-edge merchandise on schedule.

Up to now, there’s little or no proof of Intel catching up. The corporate’s struggles are significantly evident within the Knowledge Heart enterprise, the place it lags behind opponents AMD (AMD) and Nvidia (NVDA). Intel’s Q2’24 outcomes produced a 1% year-over-year income decline; a pointy distinction to its friends.

Does Intel’s Future Embody Divestments or a Buyout?

To deal with its monetary points, Intel has applied a $10 billion price discount program and just lately transformed its foundry enterprise right into a subsidiary. This restructuring goals to drive larger transparency, price financial savings, and development, however it hasn’t led me to undertake a bullish view of Intel inventory but.

The inventory gained on this announcement in September, after which additional by a take care of Amazon (AMZN) Net Providers to co-invest in a customized AI semiconductor. The corporate additionally acquired $3 billion of U.S. authorities funding to make chips for the army.

Furthermore, current stories have prompt {that a} potential $5 billion funding from Apollo International Administration (APO) could possibly be on the playing cards, and there have additionally been stories of discussions with Qualcomm (QCOM) a few doable partial or full acquisition.

Whereas the $5 billion funding could sound lofty, some analysts have prompt that it might quantity to little greater than a drop within the ocean given the capital wanted within the sector. That could be very true for Intel, given its technological lag versus friends like TSMC.

Intel Appears Cheaper than Nvidia & AMD

Regardless of all these points, stories, and turbulence, Intel seems cheaper than its friends Nvidia and AMD. Whereas INTC inventory trades at 91x ahead earnings, in keeping with analysts EPS will enhance considerably within the coming years. Resultantly, the estimated ahead price-to-earnings (P/E) ratio falls to twenty.3x for the yr ending December 2025 and to 12.6x in 2026.

By comparability, Nvidia is buying and selling at 43x ahead earnings, and 30.9x earnings for the yr ending January 2026. This determine falls to 26.3x for the yr to January 2027 and 24.3x for 2028. AMD’s valuation metrics are additionally increased, with the inventory buying and selling at 31x ahead earnings for the yr ending December 2025, and 21.8x ahead earnings for the yr ending December 2026. That means Intel is definitely considerably cheaper than its friends, albeit with out taking account of money positions.

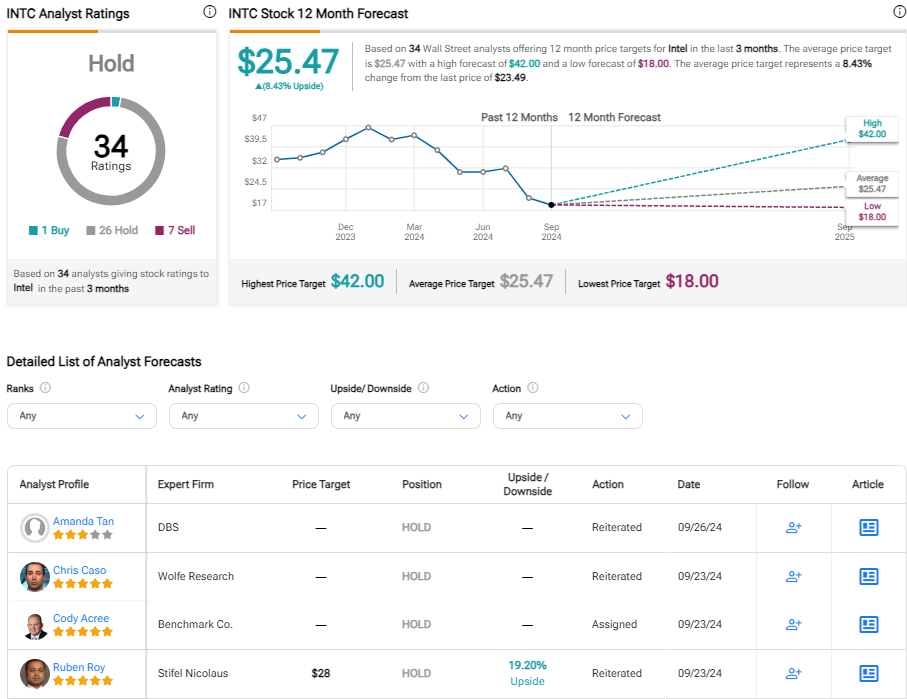

Is Intel Inventory a Purchase In line with Analysts?

On TipRanks, INTC is available in as a Maintain based mostly on one Purchase, 26 Holds, and 7 Promote scores assigned by analysts up to now three months. The common Intel inventory value goal is $25.47, implying nearly 10% potential upside.

The Backside Line on Intel Inventory

Intel’s current rally on acquisition rumors has the inventory buying and selling inside 10% of its share value goal. It’s attention-grabbing to see that the majority analysts are impartial regardless of consensus forecasts that predict a powerful restoration in earnings and really aggressive ahead valuation multiples. I consider the continuing issues about Intel’s trade relevancy compound present issues. It stays unsure how a lot help the enterprise may require to successfully compete with TSMC from a foundry perspective. I’ve a impartial view of INTC inventory.

Disclosure