The “Magnificent Seven” group of shares has been a powerhouse out there for the reason that begin of 2023, with all of them beating the S&P 500. It contains:

This assortment has had a robust run, however not each considered one of them is a robust purchase proper now, in my view. Practically each considered one of these corporations has synthetic intelligence (AI) aspirations, however my motive for purchasing three of the seven shares is centered round a a lot older follow: Promoting.

Promoting is an enormous business

If promoting is my motive to purchase a few of these shares, then Alphabet, Amazon, and Meta Platforms are those I am speaking about. This trio generates an enormous quantity of income every quarter from promoting.

|

Firm |

This autumn Promoting Income |

|---|---|

|

Alphabet |

$65.5 Billion |

|

Meta Platforms |

$38.7 Billion |

|

Amazon |

$14.7 Billion |

Information sources: Alphabet, Meta Platforms, and Amazon.

Whereas Alphabet and Meta are leaders on this class, some could also be shocked that Amazon can also be closely concerned within the advert market. In actual fact, promoting companies had been Amazon’s fastest-growing phase within the fourth quarter, rising 27% yr over yr.

Meta’s advert division additionally put up strong development figures in This autumn, with its advert income rising 24% yr over yr. Alphabet was the laggard of the trio, however this additionally is smart because of its sheer measurement. It delivered an 11% development price in This autumn.

So why are these development charges an enormous deal? Nicely, in case you rewind the clock to this time final yr, these charges weren’t practically as spectacular (apart from Amazon). The advert market struggled in early 2023 because of fears of a recession. When companies are involved a couple of potential financial downfall, they save on no matter bills they will. One of many best locations to trim is advert budgets, which negatively impacts companies like Meta and Alphabet, that are extremely concentrated on this business.

Nevertheless, the worry of imminent recession has subsided, so companies are glad to start rising their advert budgets. This is the reason ad-heavy corporations like Meta and Alphabet have seen success lately.

Amazon is a special story, as their advert income development by no means dipped like Alphabet’s or Meta’s. That is seemingly as a result of comparatively younger age of Amazon’s advert enterprise and that it is nonetheless engaged on constructing out its capabilities. When this phase matures, it’s going to seemingly show the cyclical developments that the opposite two do, nevertheless it’s in full development mode proper now.

With the advert market enhancing every quarter, all three corporations stand to learn, making them wonderful buys.

The shares are nonetheless enticing buys

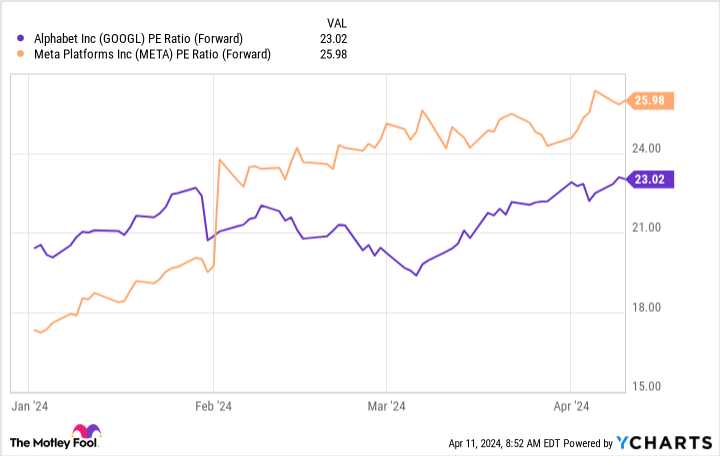

Along with a recovering advert market, these three are a few of the most attractively priced Magnificent Seven shares. My valuation metric of alternative for Alphabet and Meta is the ahead price-to-earnings (P/E) ratio, because the trailing 12 months used within the extra widespread trailing P/E ratio nonetheless contains some quarters the place the advert enterprise was down. If you happen to use this metric, it is clear these two are pretty priced.

We will use Amazon’s ahead P/E (it is at 44), however that is not honest to the enterprise as parts of the corporate (like its worldwide commerce division) aren’t worthwhile and are not anticipated to develop into absolutely worthwhile for a while. Because of this, I am going to use the price-to-sales (P/S) ratio to worth Amazon.

From this attitude, Amazon nonetheless has a strategy to go earlier than being valued on the similar ranges as 2018 by means of 2021. So, buyers can confidently purchase the inventory, realizing that it nonetheless is not again to historic valuation norms.

Promoting is a good enterprise to be in proper now, which makes this trio a unbelievable choose in 2024.

Do you have to make investments $1,000 in Alphabet proper now?

Before you purchase inventory in Alphabet, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 finest shares for buyers to purchase now… and Alphabet wasn’t considered one of them. The ten shares that made the lower may produce monster returns within the coming years.

Take into account when Nvidia made this listing on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $466,882!*

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of April 15, 2024

Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Keithen Drury has positions in Alphabet, Amazon, and Meta Platforms. The Motley Idiot has positions in and recommends Alphabet, Amazon, and Meta Platforms. The Motley Idiot has a disclosure coverage.

My High 3 “Magnificent Seven” Shares to Purchase Proper Now was initially revealed by The Motley Idiot