Let’s be trustworthy: Final yr belonged to Nvidia. The corporate, which produces high-powered, cutting-edge semiconductors which might be typically used to coach synthetic intelligence (AI) fashions, recorded a complete return of 239% in 2023. Nvidia was the best-performing inventory within the Nasdaq 100, and total it recorded one of many highest annual returns of any publicly listed inventory.

However a brand new yr has arrived. So let’s contemplate which shares would possibly dethrone Nvidia and really shine in 2024.

CrowdStrike has the wind at its again and may very well be the inventory of the yr in 2024

Jake Lerch (CrowdStrike Holdings): My selection for king of 2024 is CrowdStrike Holdings (NASDAQ: CRWD). The corporate, which gives AI-powered cybersecurity providers to its shoppers, is driving excessive after a memorable 2023.

Certainly, few shares carried out higher than CrowdStrike in 2023. Shares rallied 137% because of skyrocketing cybersecurity demand and bettering monetary fundamentals.

Let’s begin with the general demand for cybersecurity. Hacking and digital blackmail instances are on the rise. In actual fact, the previous couple of months of 2023 noticed an explosion of notable cyberattacks that introduced distinguished organizations to their knees.

In September, hackers focused hospitality and gaming big MGM in a cyberattack that precipitated huge disruptions to the corporate’s operations. A number of items of key infrastructure — together with slot machines, resort key playing cards, and ATMs — malfunctioned or had been rendered inoperable on account of the hack.

In the meantime, in October, genetics testing agency 23andMe disclosed a knowledge breach that affected at the very least 14,000 prospects. In a public relations catastrophe, delicate buyer information seems to have been compromised after which offered on the darkish internet.

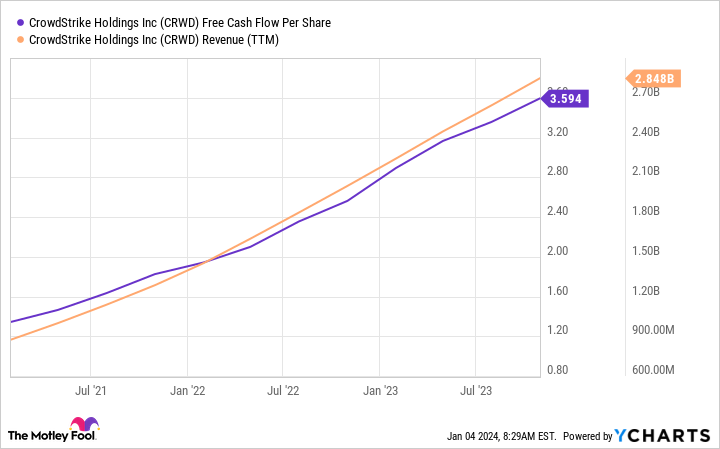

As a result of speedy improve of those real-world nightmare situations, CrowdStrike’s anti-hacking merchandise are extra in demand than ever, and its monetary metrics are hovering. Income in its most up-to-date quarter (the three months ending on Oct. 31, 2023) grew 35% year-over-year to a trailing twelve-month whole of $2.9 billion. Free money circulate jumped to $3.59/share, up from $2.89/share one yr earlier.

That stated, CrowdStrike is not for each investor, partially due to its sky-high valuation. Shares commerce at a price-to-earnings (P/E) ratio of 67, whereas its price-to-sales ratio is 21. That is excessive, even inside the red-hot tech sector.

However, CrowdStrike might nonetheless flip in a beautiful 2024 regardless of its excessive valuation. So for growth-oriented traders, CrowdStrike is unquestionably a inventory to control in 2024.

Eye-popping productiveness good points might take this inventory to the following degree

Will Healy (Palantir): Traders know Palantir (NYSE: PLTR) greatest for serving to U.S. intelligence officers discover Osama bin Laden. Since that point, the corporate has expanded into the industrial house, making use of its evaluation capabilities to enterprise issues.

Nonetheless, its success might attain new ranges on the again of its synthetic intelligence platform (AIP), which it launched final yr. The corporate’s Gotham and Foundry platforms have lengthy relied on AI, however AIP brings the capabilities of generative AI to the forefront, using giant language fashions to enhance its evaluation capabilities.

Palantir invited shoppers to AIP boot camps to indicate its energy to potential prospects, and the outcomes had been astonishing. One attendee stated they constructed 10 instances sooner with one-third of the assets. One other claimed to perform extra in sooner or later than one of many high hyperscalers had over 4 months.

With these successes, healthcare companions equivalent to HCA use it for dynamic scheduling. Additionally, Aramark, a meals and services supplier, stated AIP developed negotiating methods it might use proactively.

Admittedly, its present financials don’t mirror AIP’s potential success. The $1.6 billion in income within the first 9 months of 2023 grew 16% yearly, effectively below the 30% annual charge it had forecasted for the 2022-2024 interval again in 2021.

Nonetheless, Palantir turned worthwhile a couple of yr in the past, and within the first three quarters of 2023 it earned a internet revenue of $120 million. This implies it doesn’t have to show to debt or share dilution to fund itself.

Furthermore, traders have caught on to its potential, because the inventory has risen by round 150% during the last yr. That has taken its ahead P/E ratio to 55, making this an costly inventory by nearly any measure.

Nonetheless, the productiveness good points provided by AIP bode effectively for the inventory. Even with a excessive valuation, Palantir holds great potential to outperform the Nvidias of the world.

Monday.com is a future blue-chip inventory in enterprise software program

Justin Pope (Monday.com): Enterprise software program is a ruthlessly aggressive house the place firms typically sacrifice earnings for income development. However ultimately the tide goes out, the market crashes, and people unable to show a revenue by no means once more see their former highs. Monday.com (NASDAQ: MNDY), down over 60% from its excessive, is attempting to show it might make a comeback.

Monday.com sells software-as-a-service that helps staff collaborate and handle initiatives. That is a crowded house with deep-pocketed (Microsoft) and rising (Asana) competitors. But the corporate has managed to maintain elevating its recreation to new ranges.

The corporate has greater than doubled its annual income over the previous a number of years, approaching $700 million. Over 2,000 enterprise accounts spend over $50,000 on the product yearly. The product works for small organizations too, so there’s room for long-term development as Monday.com’s prospects develop and spend extra over time.

However in the end, traders need to see earnings — and Monday.com has these too.

After the corporate’s money circulate roughly broke even for a number of quarters, free money circulate exploded to the optimistic in 2023. Its $179 in trailing 12-month money circulate is already 26% of its gross sales, a large leap in profitability in a short while. That bodes effectively for bottom-line earnings (internet revenue). Monday.com turned GAAP optimistic in Q3, so buckle up for speedy earnings development in 2024 and past.

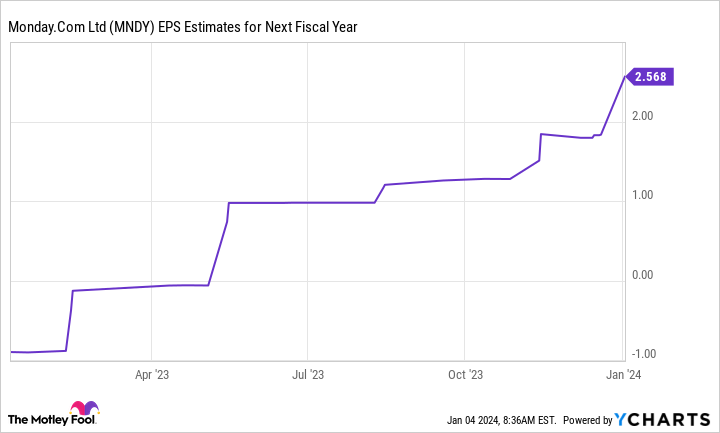

Consensus analyst estimates name for earnings per share (EPS) of $2.57 in 2024, valuing the inventory at a ahead P/E of 67. For a enterprise that might compound earnings at a speedy tempo for a number of years, that is a really cheap value to pay. Bear in mind, the inventory nonetheless sits over 60% off its excessive over two years in the past regardless of being a lot greater and extra worthwhile than again then. Monday.com’s return to its highs appears extra like a matter of time.

Must you make investments $1,000 in CrowdStrike proper now?

Before you purchase inventory in CrowdStrike, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 greatest shares for traders to purchase now… and CrowdStrike wasn’t one in all them. The ten shares that made the lower might produce monster returns within the coming years.

Inventory Advisor gives traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

See the ten shares

*Inventory Advisor returns as of December 18, 2023

Jake Lerch has positions in CrowdStrike and Nvidia. The Motley Idiot has positions in and recommends Asana, CrowdStrike, HCA Healthcare, Microsoft, Monday.com, Nvidia, and Palantir Applied sciences. The Motley Idiot has a disclosure coverage.

Prediction: Nvidia Was the Star of 2024, However These 3 Shares May Outshine It in 2024 was initially revealed by The Motley Idiot