This 12 months’s robust rally has stuttered over the previous few weeks. August has typically seen elevated volatility and declines in the principle market indexes. However that hasn’t affected a primary reality of the monetary markets: shares are people, they usually rise and fall for idiosyncratic causes. Traders ought to at all times examine beneath the hood, to search out out if a cut price value represents a very good purchase.

That examine may be tough, nevertheless, as there are reams of information to kind. Happily, buyers can at all times flip to the Sensible Rating, an AI-powered knowledge assortment and collation device, primarily based on the TipRanks database, that charges each inventory based on a set of things confirmed by historical past to match up with future outperformance. Search for shares that mix the very best Sensible Rating, a ‘Excellent 10,’ with a pullback in share value – that’s the place the true bargains could also be hiding.

We will get began with a have a look at two Robust Purchase shares that characteristic each lowered share costs and a ‘Excellent 10’ from the Sensible Rating. These are shares which have attracted analyst consideration; are they best for you?

Shift4 Funds (FOUR)

The primary ‘Excellent 10’ inventory on our listing is Shift4 Funds, a tech agency working within the cost processing enterprise. The Allentown, Pennsylvania-based agency offers companies throughout a variety of industries, and counts some huge names amongst its buyer base: Finest Western Lodges, Applebee’s, the Utah Jazz, Gold’s Fitness center. General, the corporate boasts greater than 200,000 clients and over 7,000 gross sales companions, and processes greater than 3.5 billion transactions value greater than $200 billion yearly.

In an vital announcement, earlier this month Shift4 indicated that it’s nearing the closure of its Finaro acquisition. The $525 million transfer will give Shift4 entry to Finaro’s European processing community. The deal was anticipated to have closed in March of this 12 months, however was held up resulting from ‘regulatory necessities;’ it’s now anticipated to shut in Q3/early This autumn.

The corporate reported its 2Q23 outcomes early this month, and confirmed a collection of positive aspects, together with year-over-year income and earnings development, that beat expectations. On the prime line, the corporate reported revenues of $637 million, up 26% year-over-year and virtually $4 million higher than had been anticipated. The underside line determine, a non-GAAP adjusted EPS of 74 cents per share, was 22 cents forward of the estimates, and greater than triple the year-ago outcome. The corporate noticed a 59% y/y enhance in end-to-end cost quantity, and a 61% y/y enhance in gross revenue.

Regardless of the robust outcomes, the inventory has been by a little bit of a selloff lately, having retreated by 19% throughout August. For Raymond James analyst John Davis, the inventory’s value decline makes it a horny cut price purchase. He writes in his protection, “We see upside to FY24 Road estimates, assuming Finaro does in actual fact shut, given the Road is implying simply ~22% natural income development (~800 bp decel) and ~80 bp of EBITDA margin enlargement… The inventory is now buying and selling close to trough valuation ranges at simply 10x FY24E EBITDA and a ~20% low cost to the S&P 500 on EV/EBITDA. As such, we view the current weak point as a compelling entry level and advocate buyers provoke or add to positions.”

As such, Davis lately upgraded his stance on FOUR, bumping it from Impartial to Outperform (a Purchase). The analyst enhances his new ranking with a $74 value goal, implying a one-year upside potential of 33% from present ranges. (To look at Davis’s monitor report, click on right here.)

Shift4 has picked up 17 current analyst critiques, together with 16 to Purchase towards simply 1 to Maintain, to again up its Robust Purchase consensus ranking. The shares are buying and selling for $55.76, and the $83.75 common value goal suggests it’s going to acquire 50% within the 12 months forward. (See Shift4 Funds’ inventory forecast.)

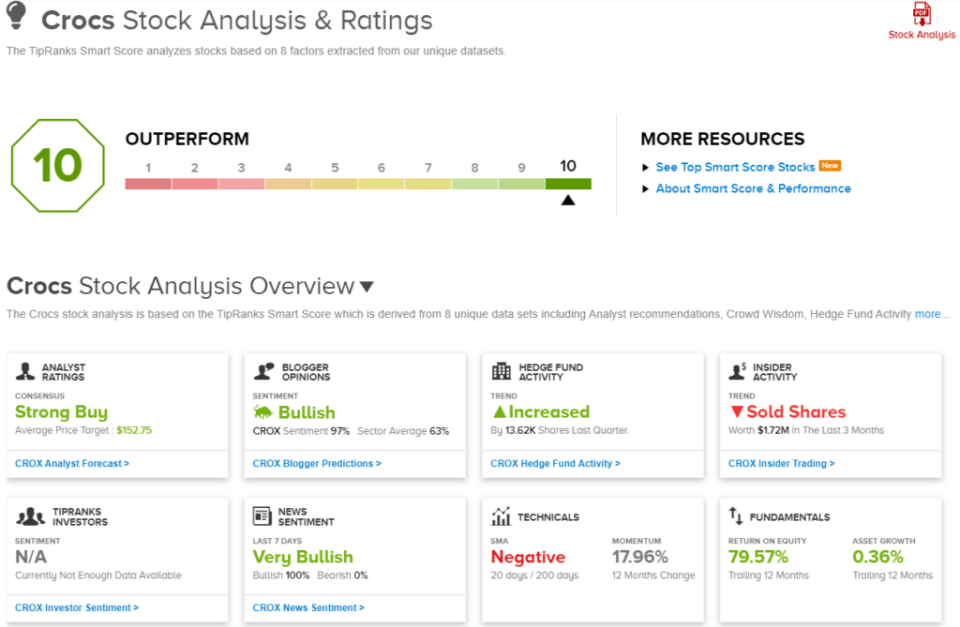

Crocs (CROX)

Subsequent up is Crocs, a recognizable model title in footwear. The corporate constructed its title on its eponymous foam clogs that grew to become such a success within the early 2000s. At present, the corporate provides a variety of footwear traces, from the froth clogs to flip flops to sandals, boots, and cozy work sneakers. The corporate even markets a line of sneakers designed for healthcare professionals who spend lengthy days on their toes.

By the numbers, Crocs has constructed itself an empire. The corporate has bought greater than 850 million pairs of sneakers because it hit the markets in 2002. Crocs employs over 5,900 folks and has a presence in 85 international locations world wide, and makes over 2 billion gross sales yearly. Collectively, all of this places Crocs among the many world’s prime ten athletic footwear manufacturers.

Earlier this summer time, Crocs reported its 2Q23 monetary numbers – and confirmed a report income determine of $1.072 billion. This was up 11% y/y, and was $29.2 million forward of the forecast. On the backside line, Crocs reported earnings of $3.59 per share by non-GAAP measures. This marked an 87-cent per share enhance over the prior 12 months’s Q2 earnings, and was 61 cents per share higher than anticipated.

Nonetheless, buyers didn’t just like the outlook. For Q3, the corporate sees adj. earnings hitting the vary between $3.07 to $3.15 per share, on the midpoint, under consensus at $3.12. Furthermore, with Q3 revenues anticipated to develop round 3% to five% y/y, there are issues about slowing development. The result’s a inventory that has been on the backfoot because the Q2 print, down by 21%.

However, Jim Duffy, 5-star analyst from Stifel, takes an upbeat view of CROX, basing his stance on web positives from the earnings outcomes and on the corporate’s model power, writing, “FY2Q outcomes have been a blended bag however positives outweigh the damaging and the [pullback] in shares presents a chance. Market disappointment displays the shortfall from HEYDUDE wholesale (~15% of world income) however appears previous optimistic developments for the Crocs model (~75% of world income). Particular elements showcasing improved steadiness and growing our confidence into FY24 embrace 1) Crocs N. America model power and product diversification, 2) Crocs worldwide power led by +40% DTC comp and Asia/China, and three) debt discount bringing web leverage <1.7X.”

Duffy goes on to level out that Crocs has a strong basis for future positive aspects: “Revenue pool diversification, improved steadiness sheet optionality, and a really forgiving valuation enhance our confidence in threat adjusted return prospects for CROX shares.”

At backside, all of this helps Duffy’s Purchase ranking, whereas his goal value of $130 factors towards a 36% acquire on the one-year time horizon. (To look at Duffy’s monitor report, click on right here.)

Of the 9 current analyst critiques on CROX, 7 are to Purchase and a pair of to Maintain, sufficient to usher in a Robust Purchase consensus ranking. The inventory’s $95.56 share value and $152.75 common value goal recommend a strong 60% upside over the subsequent 12 months. (See Crocs’ inventory forecast.)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched device that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely vital to do your individual evaluation earlier than making any funding.