Traits come and go however the newest craze to take Wall Avenue by storm is proving fairly persistent. AI hype has been all the trend this 12 months and shares with publicity to generative AI and LLMs (massive language fashions) have been reaping the advantages.

A lot so, that Wall Avenue’s finest analyst thinks it’s time to alter tune on a lot of them. Surveying the SemiCap house, Needham analyst Quinn Bolton is confronted by a plethora of names boasting lofty valuations with little room left to run from right here.

“With SemiCap shares up meaningfully on the AI hype however with AI unlikely to drive a big improve in WFE spending, we imagine many SemiCap shares are overbought within the near-term,” the 5-star analyst stated. “In our opinion, buyers might want to look out to 2025 and 2026 and the subsequent WFE up cycle to find out if there’s sufficient earnings energy within the upturn to justify shopping for the shares at present ranges.”

Given the above, Bolton has downgraded the scores of a number of SemiCap shares. That stated, not all SemiCap shares are priced to perfection. Bolton, who boasts a 72% success price on his inventory suggestions and a mean return of 39%, presently occupies the highest spot amongst the Avenue’s analysts, so it’s truthful to say he has a really feel for this recreation. And he thinks two SemiCap equities, specifically, are nonetheless ripe for the choosing. Let’s take a more in-depth look.

ACM Analysis (ACMR)

The primary inventory we’ll have a look at is ACM Analysis, a frontrunner within the superior expertise and manufacturing instruments required by the chip trade within the manufacturing of silicon wafers. This can be a deeper stage of a necessary trade, and ACM Analysis has traces of instruments for moist processing, electrochemical plating, stress-free sprucing, and different important chip manufacturing processes. Put merely, the businesses making the chips that energy AI methods couldn’t even start their work with out ACM’s instruments.

Along with the high-tech instruments, ACM Analysis additionally provides strong buyer assist, which is maintained via the lifetime of the corporate’s gear merchandise. ACM Analysis will assist its clients set up its machines, after which work with them to optimize methods and forestall issues, avoiding bottlenecks in chip manufacturing. The corporate’s assist actions embrace software program, apps, and spare elements and repair, regardless of the place the shopper is situated.

The demand for silicon semiconductor chips has been useful for ACM Analysis, which is clearly seen within the firm’s final quarterly report for 1Q23. On the high line, ACMR confirmed revenues of $74.26 million, marking a 76% year-over-year improve and surpassing the forecast by over $5.5 million. The agency’s backside line earnings, of 15 cents per share by non-GAAP measures, got here in 16 cents per share forward of expectations. The corporate additionally caught to its income information for fiscal 12 months 2023, calling for gross sales within the vary between $515 million to $585 million. The consensus estimate was $540.58 million.

Quinn Bolton likes this firm’s stability sheet, as he famous in his latest evaluation of the shares. Establishing his stance on ACMR, he wrote: “Because the quickest rising SemiCap inventory in our protection with ~$400MM in money and little or no debt, we imagine a 12.5x a number of is greater than truthful. The inventory is presently receiving little consideration from buyers on account of its high-exposure to China. Nonetheless, we imagine this ACMR sentiment will change over time as its development proves too troublesome to disregard.”

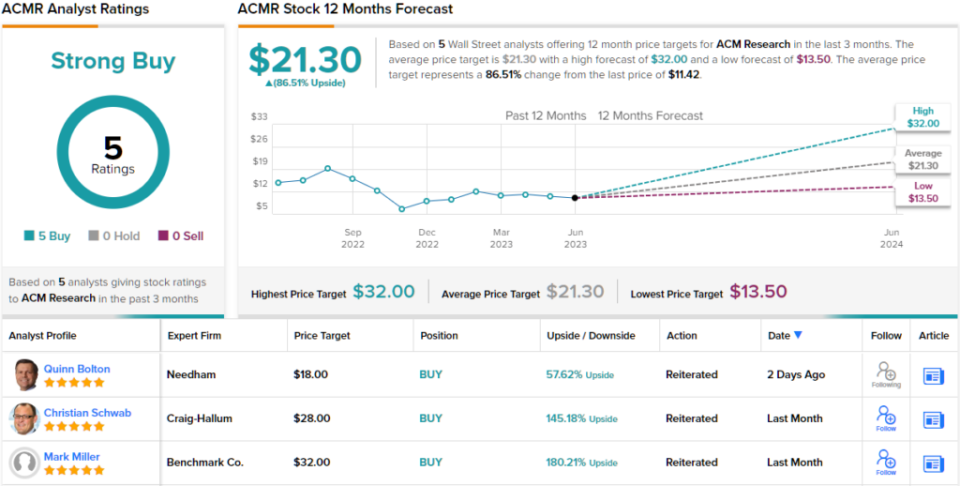

Trying forward, Bolton goes on to price ACMR as a Purchase, with an $18 worth goal implying a one-year upside potential of 59%.

Like Bolton, different analysts additionally take a bullish method. ACMR’s Sturdy Purchase consensus ranking breaks down into 5 Buys and 0 Holds or Sells. Given the $21.30 common worth goal, the upside potential lands at 86%. (See ACMR inventory forecast)

Cohu, Inc. (COHU)

The second of Bolton’s picks that we’re is Cohu, a number one producer of check and inspection gear utilized in chip fabrication traces. The merchandise supplied by Cohu play a significant position in making certain meticulous high quality management all through the chip manufacturing course of.

Cohu has established itself as a key participant within the chip-testing area of interest, with a broad portfolio of check gear and companies designed to fulfill the wants of backend semiconductor producers. The corporate describes itself as a ‘one-stop store’ for a variety of testing options, together with dealing with gear, thermal subsystems, and imaginative and prescient inspection & metrology.

The corporate doesn’t cease with chip makers, nevertheless. Cohu has solidified its presence within the high-tech testing enterprise by increasing its choices, with check and high quality management gear for IoT, industrial & medical, mobility, automotive, computing & community, and shopper product purposes. The corporate has come a great distance from its 1947 founding.

Cohu’s final monetary launch, nevertheless, for 1Q23, confirmed some blended outcomes. The corporate’s income was down 9.3% y/y, to $179.37 million, and missed the forecast by $0.92 million. Cohu’s non-GAAP gross margin was up, nevertheless, from 46.1% in 1Q22 to 48.2% in 1Q23. This helped the bottom-line efficiency, as adj. EPS of $0.56 beat the forecast by $0.02.

The constructive metrics attracted Bolton’s consideration, and he wrote of the inventory: “Cohu’s NG GM is displaying resiliency even at a decrease income stage, and we proceed to imagine a robust GM will assist assist shares close to present ranges. Strong recurring income, increasing manufacturing within the Philippines, greater handler margins, and blend is enabling robust GM. Elevated prices had a 29bps affect on GM and can proceed via 2023.”

“Notably,” the highest analyst went on so as to add, “COHU acquired a multi-unit $5MM SiC order for check automation and inspection. COHU believes SiC will make up ~2.5% of gross sales in 2023. Nonetheless, we imagine COHU’s close to and long-term alternative in SiC is presently underappreciated. We count on COHU’s SiC income to develop quicker than the top-line in coming years.”

Taking this optimistic stance ahead, Bolton provides COHU inventory a Purchase ranking and units a $52 worth goal, indicating confidence in a 29% upside on the one-year time horizon.

General, the Wall Avenue consensus on COHU is a Sturdy Purchase, based mostly on 4 analyst evaluations together with 3 Buys and 1 Maintain. The shares are promoting for $40.12, and the common worth goal of $42.75 implies a one-year upside of 6.5% for the inventory. (See COHU inventory forecast)

To search out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Greatest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally essential to do your personal evaluation earlier than making any funding.