Software Company Could Be the Next Palantir")

For fairly a while, the view surrounding Palantir Applied sciences (NYSE: PLTR) was caught someplace between a generational software program developer or an “AI imposter,” relying on whom you ask. One of many greatest causes for this polarizing viewpoint is that many buyers merely don’t perceive what Palantir truly does.

Juxtaposing business buzzwords similar to “AI” and “data-driven insights” will solely get you up to now. In some unspecified time in the future, a enterprise must show that it is advertising and marketing ways are bearing fruit. And, in actual fact, over the previous yr Palantir has witnessed a brand new wave of development due to its lineup of information analytics software program platforms.

The corporate has not solely accelerated its prime line, however it’s additionally been persistently increasing revenue margins and has transitioned from a cash-burning operation to a worthwhile enterprise. Lately, Palantir turned a member of the S&P 500 and is working intently with among the tech sector’s largest incumbents, together with Microsoft and Oracle.

Right now, one other firm on this sector additionally deserves a better look: ServiceNow (NYSE: NOW). Ever heard of it? I’ll element how ServiceNow is quietly disrupting the world of enterprise software program — much like what Palantir has finished. Furthermore, I am going to discover how AI is enjoying a serious function within the firm’s present development trajectory and assess if now could be a profitable alternative to scoop up shares.

What does ServiceNow do?

A few yr in the past, ServiceNow CEO Invoice McDermott sat down for an interview with David Rubenstein — a personal fairness investor and former coverage advisor throughout President Jimmy Carter’s administration.

When requested about what ServiceNow truly does, McDermott merely referred to the corporate because the “IT spine” for companies trying to construct out digital infrastructure. Whereas I admire the metaphor right here, I am going to admit that this rationalization continues to be just a little obscure.

Let us take a look at an instance to higher perceive the ServiceNow platform. From finance, gross sales and advertising and marketing, operations, human sources, and IT administration, firms have a separate division for nearly the whole lot. Consequently, organizational workflows could be slow-moving, and staff could be left ready for an optimum answer for hours and even days.

That is the place ServiceNow is available in. The corporate presents a complete suite of SaaS-based instruments and providers aimed to assist streamline generic inefficiencies inside organizations. This helps staff and staff members higher observe the standing of essential points or initiatives, in the end driving increased productiveness.

How is AI a tailwind for ServiceNow?

Like many software program firms, ServiceNow is trying to journey the AI wave. And on the floor, the corporate appears to be doing a superb job. Since AI turned the speak of the city, ServiceNow has signed some high-profile partnerships with Microsoft, IBM, and Nvidia, simply to call a couple of. However as I alluded to, advertising and marketing strategic alliances and doing extremely publicized interviews is just one a part of the equation.

How is ServiceNow’s enterprise truly performing? Fairly solidly, if you happen to ask me.

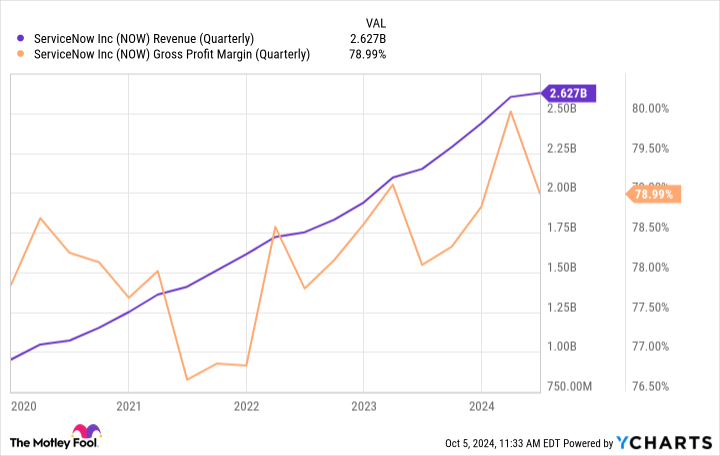

As depicted within the chart, ServiceNow’s income and gross revenue margin have been rising considerably over the past a number of years. Diving a bit deeper right here, take a look at the expansion traits beginning in 2023 — roughly the interval throughout which AI began to land on extra radars.

Simply over the past 20 months or so, ServiceNow’s income line begins to witness a noticeably steeper slope, whereas revenue margins concurrently broaden. What’s even higher is the mixture of accelerating gross sales and wider margins is resulting in constant profitability — each from a internet revenue and free money movement perspective.

Is ServiceNow inventory a purchase proper now?

Though ServiceNow is persistently worthwhile, the magnitude of its internet revenue and money movement fluctuates fairly a bit. Keep in mind, ServiceNow is a development firm, so it’s always reinvesting extra earnings again into the enterprise.

Because of this, utilizing profit-based valuation metrics similar to price-to-earnings (P/E) or price-to-free money movement (P/FCF) aren’t completely helpful. As an alternative, I’m going to have a look at the ratio between enterprise worth and income.

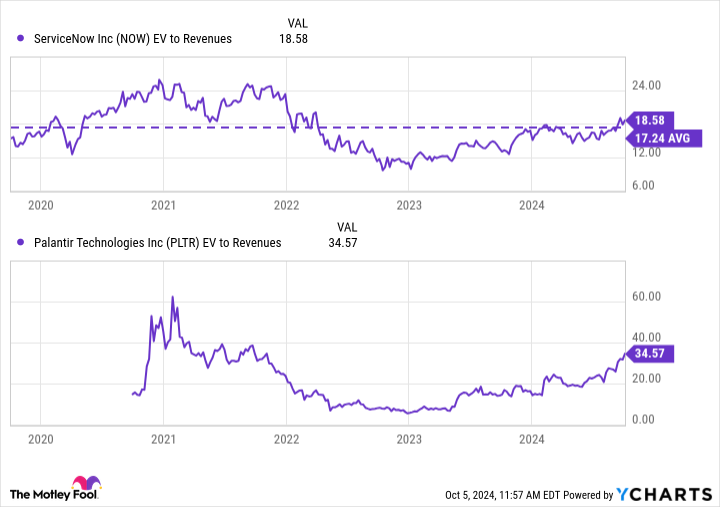

Proper now, ServiceNow trades at an EV-to-sales a number of of 18.6 — primarily consistent with its five-year common. However if you happen to take a better take a look at the overarching traits, there’s a lot that may be gathered from these charts.

Following a quick pop in 2020, each ServiceNow’s and Palantir’s valuation multiples compressed fairly considerably between 2021 and 2023. A lot of this was attributable to macro components similar to inflation and rising rates of interest, and their toll on the enterprise software program market as an entire.

Nonetheless, because the AI daybreak come into sight round 2023, ServiceNow and Palantir began witnessing some valuation growth. What’s peculiar is that even with this valuation growth, ServiceNow’s EV-to-revenue is mainly again to the place it was a number of years in the past.

When you think about the truth that ServiceNow is a a lot bigger, worthwhile enterprise as we speak in comparison with 2020, I believe that there’s an argument to be made that the inventory is undervalued — regardless of the gradual uptick in valuation over the past two years.

To me, the market is starting to catch on to ServiceNow, roughly because it did with Palantir. Nonetheless, I nonetheless suppose ServiceNow is just not but totally appreciated concerning how it’s enjoying an integral function on the crossroads of AI and enterprise software program.

For these causes, I believe now is a superb time to purchase ServiceNow inventory, and I see the corporate following a really related narrative and trajectory to that of Palantir because the AI narrative continues to take form.

Must you make investments $1,000 in ServiceNow proper now?

Before you purchase inventory in ServiceNow, take into account this:

The Motley Idiot Inventory Advisor analyst staff simply recognized what they consider are the 10 finest shares for buyers to purchase now… and ServiceNow wasn’t considered one of them. The ten shares that made the reduce may produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… if you happen to invested $1,000 on the time of our advice, you’d have $814,364!*

Inventory Advisor gives buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of October 7, 2024

Adam Spatacco has positions in Microsoft, Nvidia, and Palantir Applied sciences. The Motley Idiot has positions in and recommends Microsoft, Nvidia, Oracle, Palantir Applied sciences, and ServiceNow. The Motley Idiot recommends Worldwide Enterprise Machines and recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

Prediction: This Synthetic Intelligence (AI) Software program Firm Might Be the Subsequent Palantir was initially printed by The Motley Idiot