LONDON, Oct 27 (Reuters) – Having hiked mortgage charges after political turmoil drove up the price of borrowing, British banks are actually reducing dwelling mortgage costs, albeit slowly, as markets calm since Liz Truss’s authorities collapsed and Rishi Sunak took energy.

Market chaos unleashed by Truss’s huge unfunded tax-cutting plans in late September led lenders to withdraw round 1,700 mortgage merchandise within the area of per week, earlier than reintroducing them at charges 1-2 share factors greater.

However as markets have stabilised and borrowing prices have fallen, the trickle of mortgage fee cuts has lagged behind.

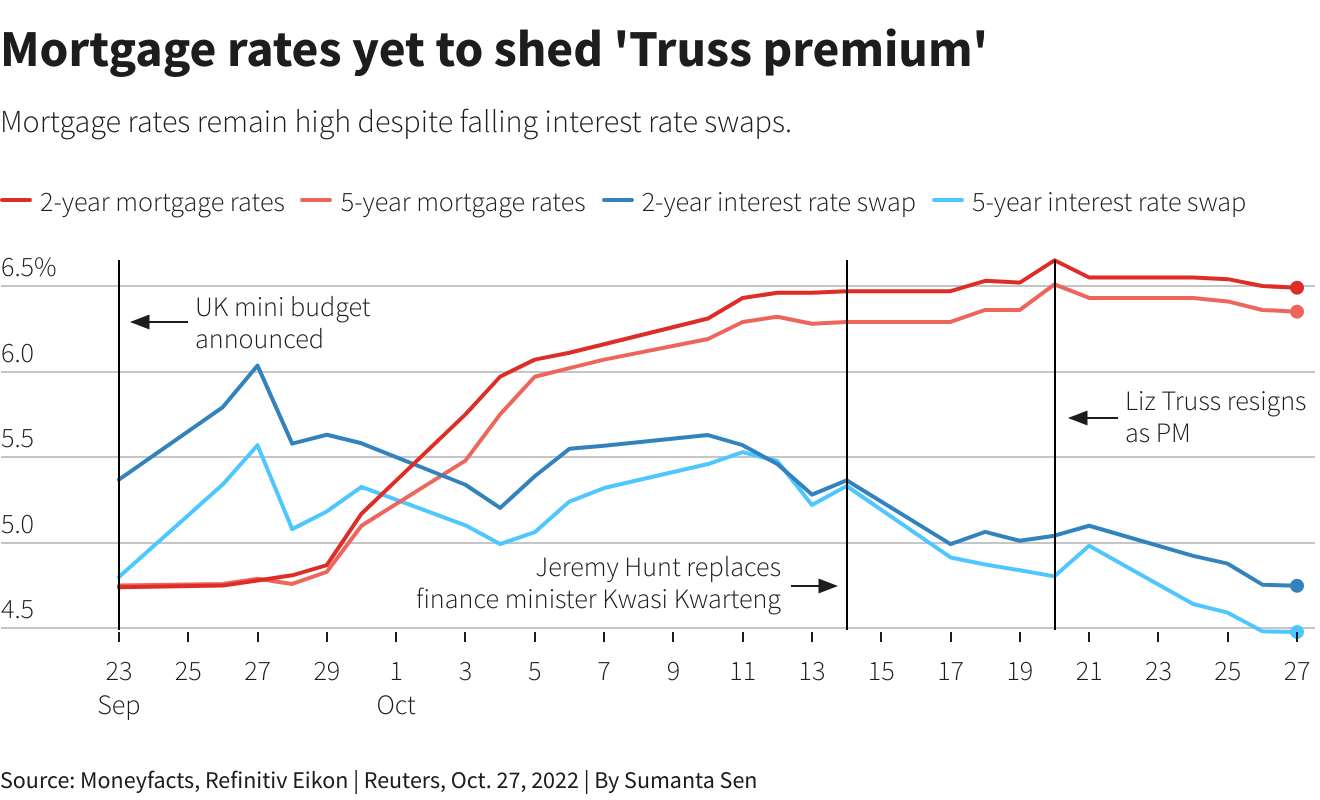

A number of key rate of interest swaps – merchandise that lenders use to lock in future charges earlier than pricing fixed-rate mortgages – have fallen by between 1.3 and 1.4 share factors from their Truss-administration peak, Refinitiv knowledge reveals.

In contrast, common charges on two-year and five-year fixed-rate mortgages have fallen simply 0.16 share factors, Moneyfacts knowledge reveals.

“Lenders are in a position to get away with not passing cheaper charges on to mortgage clients, aided by the failure of Britain’s over-concentrated banking system to operate like a aggressive market,” mentioned Simon Youel, head of coverage and advocacy at Constructive Cash, which campaigns for a fairer monetary system.

A spokesperson for banking foyer group UK Finance mentioned the mortgage market was aggressive, including that lenders used a spread of standards to find out pricing.

Housing consultants say additional value drops ought to comply with based mostly in the marketplace shift since Truss and her workforce’s departure.

FIXED RATES

Mortgage brokers say fixed-rate mortgage charges usually lag modifications in swap charges, a pattern which may very well be exacerbated this time as lenders deal with reintroducing merchandise. The variety of fixed-rate choices remains to be down practically 1 / 4 from pre-Truss ranges, based on Moneyfacts.

Lenders are beneath strain to indicate they’re treating clients pretty in the price of residing disaster, and have already confronted criticism from shopper teams for not passing sufficient Financial institution of England fee rises to savers.

Additionally they face the specter of a possible tax raid from Sunak’s authorities because it appears to be like to plug a niche within the nation’s funds.

Britain’s housing market has boomed for the reason that preliminary affect of the COVID-19 pandemic, however squeezed family budgets exacerbated by extra expensive dwelling loans appears to be like set to plunge it right into a downturn.

The nation’s largest mortgage lender Lloyds (LLOY.L), proprietor of the Halifax model, mentioned on Thursday it anticipated a mortgage market slowdown subsequent yr, and for home costs to drop 8%.

After years of low-cost borrowing, mortgage costs had been climbing this yr because the Financial institution of England ratcheted up benchmark charges. However this accelerated after Truss’s finance minister Kwasi Kwarteng laid out a disastrous “mini finances” on Sept. 23.

The typical fee on a two-year mounted fee mortgage leapt as excessive as 6.65% by Oct. 20, Moneyfacts knowledge reveals, whereas previous to the finances it was 4.74%. Opposition politicians labeled the soar a “Truss premium” on mortgages.

The typical two-year fee has since edged down 0.16 share factors to six.49% as of Thursday. 5-year mortgage charges have adopted the same sample, Moneyfacts knowledge reveals.

FISCALLY MODERATE

Nevertheless, market pricing on future benchmark charges has fallen considerably since peaking in late September, Refinitiv knowledge reveals, as markets have warmed to a extra fiscally reasonable finance minister Jeremy Hunt and prime minister Sunak.

Two-year rate of interest swaps have fallen from a peak of 6.1% on Sept. 28 to 4.7% as of Thursday, based on Refinitiv knowledge, tremendously outpacing the dip in mortgage charges.

It is a comparable image for five-year charges. Cash market five-year swap charges are down 1.3 share factors from their post-budget peak to 4.4%, whereas the typical five-year mounted mortgage is up to now simply 0.16 share factors cheaper than the Truss peak, down from 6.51% to six.35%.

“There have been a few indicators of reductions, some are important,” mentioned Mike Learn, monetary adviser at mortgage dealer Prospect Tree Monetary Companies. “We most likely want a number of extra weeks to see it filtering although.”

Santander’s (SAN.MC) British arm has been among the many first lenders to decrease mortgage charges this week, reducing some mounted charges by as a lot as 0.5 share factors, based on Moneyfacts, whereas Yorkshire Constructing Society’s Accord model lower charges by as much as 0.53 share factors.

Barclays (BARC.L) finance chief Anna Cross informed analysts after the financial institution’s earnings that the mortgage market was aggressive and pricing ought to comply with market situations.

Lenders have mentioned growing mortgage charges in current weeks was the rational factor to do as risky cash markets priced a lot greater future rates of interest final month, so greater costs had been wanted to keep away from them writing dwelling loans at a loss.

Lloyds mentioned on Thursday its future pricing would partly be decided by strikes in cash markets.

“We’ll need to see how these fare on a sustainable foundation going ahead,” the financial institution’s finance chief William Chalmers informed reporters. “We are going to do our greatest to reply to clients in probably the most applicable method.”

Reporting by Iain Withers and Lawrence White; Modifying by David Holmes

: .